Entity Annual Report Indiana Form in PDF

Entity Annual Report Indiana Form in PDF

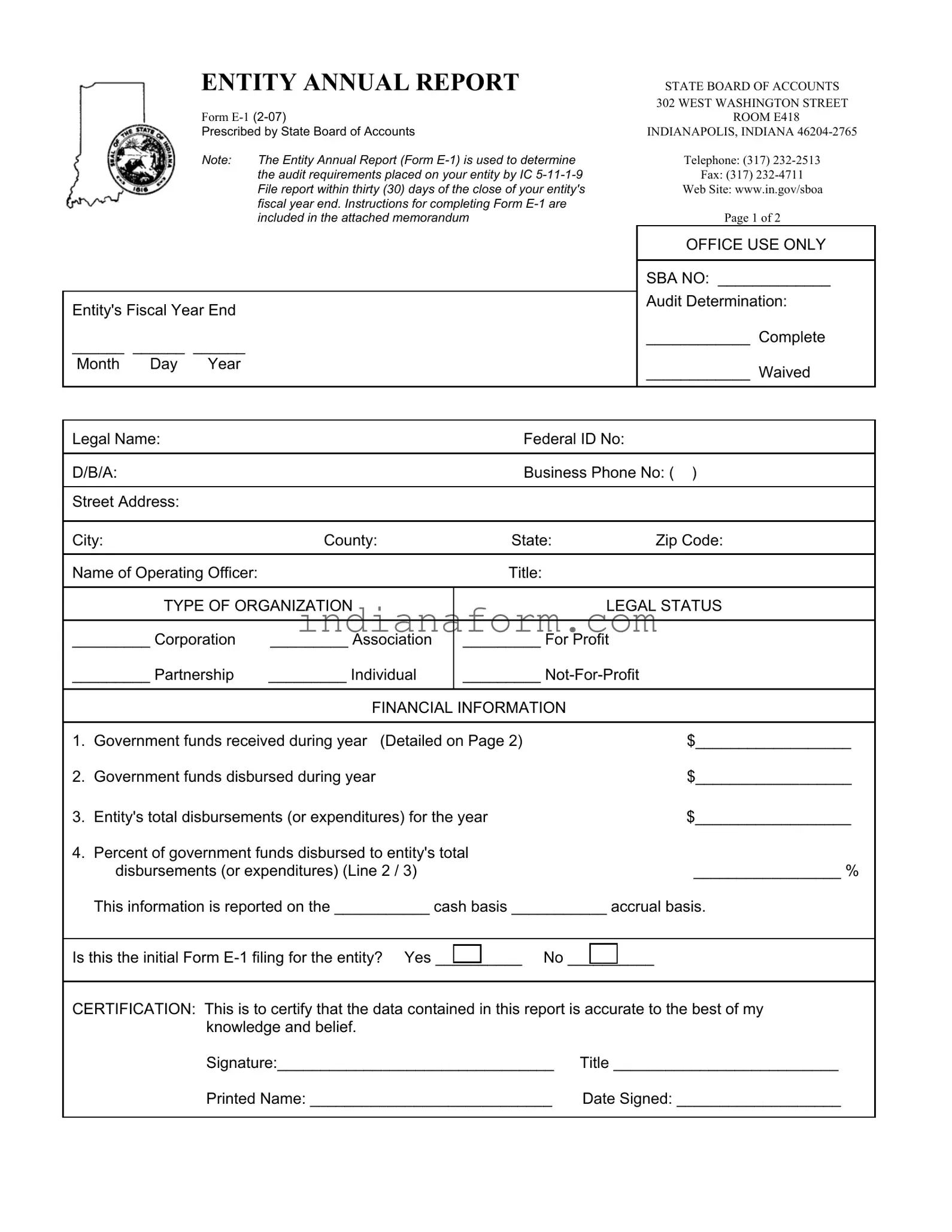

In Indiana, entities must navigate the legal requirements of financial reporting, a task encompassed by the Entity Annual Report (Form E-1), as prescribed by the State Board of Accounts. Located at 302 West Washington Street in Indianapolis, this form serves a pivotal role in determining the scope of audit requirements under IC 5-11-1-9, ensuring transparency and accountability in the financial operations of various organizations. Required to be filed within thirty days following the fiscal year-end, the Form E-1 encompasses significant data, including the entity's legal status, type of organization, detailed financial transactions involving government funds, and a certification of accuracy by the operating officer. It also asks for the organizational structure, purpose, and history of independent audits, thereby offering a comprehensive overview for the State Board of Accounts to evaluate the need for further auditing. This process not only aids in the oversight of entities but also enhances the integrity of financial management practices within the state. With instructions provided for completing the form, entities are guided through reporting on both a cash and accrual basis, highlighting the importance of precise and thorough financial documentation.

ENTITY ANNUAL REPORT |

STATE BOARD OF ACCOUNTS |

|

|

|

302 WEST WASHINGTON STREET |

Form |

ROOM E418 |

|

Prescribed by State Board of Accounts |

INDIANAPOLIS, INDIANA |

|

Note: |

The Entity Annual Report (Form |

Telephone: (317) |

|

the audit requirements placed on your entity by IC |

Fax: (317) |

|

File report within thirty (30) days of the close of your entity's |

Web Site: www.in.gov/sboa |

|

fiscal year end. Instructions for completing Form |

|

|

included in the attached memorandum |

Page 1 of 2 |

Entity's Fiscal Year End

______ ______ ______

Month Day Year

OFFICE USE ONLY

SBA NO: _____________

Audit Determination:

____________ Complete

____________ Waived

Legal Name: |

|

Federal ID No: |

|

|

|

|

|

||

D/B/A: |

|

Business Phone No: ( ) |

||

|

|

|

|

|

Street Address: |

|

|

|

|

|

|

|

|

|

City: |

County: |

State: |

Zip Code: |

|

|

|

|

|

|

Name of Operating Officer: |

|

Title: |

|

|

|

|

|

||

|

TYPE OF ORGANIZATION |

LEGAL STATUS |

||

|

|

|

|

|

_________ Corporation |

_________ ASSOCIATION |

_________ For Profit |

|

|

_________ Partnership |

_________ INDIVIDUAL |

_________ |

|

|

|

|

|

|

|

|

|

FINANCIAL INFORMATION |

|

|

|

|

|

||

1. |

Government funds received during year (Detailed on Page 2) |

$__________________ |

||

2. |

Government funds disbursed during year |

|

$__________________ |

|

3. |

Entity's total disbursements (or expenditures) for the year |

$__________________ |

||

4. Percent of government funds disbursed to entity's total |

|

|

|

||

disbursements (or expenditures) (Line 2 / 3) |

_________________ % |

||||

This information is reported on the ___________ cash basis ___________ accrual basis. |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Is this the initial Form |

__________ No |

__________ |

|||

|

|

|

|

|

|

CERTIFICATION: This is to certify that the data contained in this report is accurate to the best of my |

|||||

knowledge and belief. |

|

|

|

||

Signature:________________________________ |

Title __________________________ |

||||

Printed Name: ____________________________ |

Date Signed: ___________________ |

||||

Page 2 of 2

DETAIL OF GOVERNMENT FUNDS RECEIVED

List the government funds received during the year by agency, address, program title and amount received. Attach additional sheets if necessary.

GOVERNMENT AGENCY

ADDRESS

PROGRAM TITLE

AMOUNT RECEIVED

Date organization was founded: _________________________________________________________________

Describe organization's purpose:_________________________________________________________________

___________________________________________________________________________________________

Describe organizational governing structure:________________________________________________________

___________________________________________________________________________________________

Have you ever been audited by an Independent Public Accountant (IPA)? Yes ___________ No ___________

If so, what was the last fiscal year audited? ________________________________________________________

Name and address of IPA that conducted audit: _____________________________________________________

___________________________________________________________________________________________

| Fact | Detail |

|---|---|

| Form Name | Entity Annual Report (Form E-1) |

| Prescribed by | State Board of Accounts |

| Address | 302 West Washington Street, Room E418, Indianapolis, Indiana 46204-2765 |

| Contact Information | Telephone: (317) 232-2513, Fax: (317) 232-4711, Web Site: www.in.gov/sboa |

| Deadline for Filing | Within thirty (30) days of the close of the entity's fiscal year end |

| Governing Law | IC 5-11-1-9 |

| Types of Organization Legal Status Available | Corporation, Association, For Profit, Partnership, Individual, Not-For-Profit |

| Reporting Basis | Cash basis, Accrual basis |

| Audit Requirement Determination | Based on the audit requirements placed on the entity by IC 5-11-1-9 |

Filing the Entity Annual Report in Indiana is a critical process for any entity operating within the state. This report allows the State Board of Accounts to assess your audit requirements under IC 5-11-1-9. Filling it out correctly and on time ensures compliance with state laws and contributes to the transparent operation of your entity. The following steps are designed to guide you through each section of the form to ensure accuracy and completeness.

Once all the information is filled in, review the report for accuracy and completeness. It's important that the information provided correctly reflects your entity's operations and financial status. After review, submit the report within thirty (30) days of the close of your entity's fiscal necklace end, ensuring your compliance with Indiana state regulations. Filing this report is not just a legal requirement; it also provides valuable insight into the financial operations of your entity that can aid in future planning and accountability.

What is the Entity Annual Report in Indiana?

The Entity Annual Report, known as Form E-1, is a document required by the State Board of Accounts in Indiana. It collects financial information and other details about an entity to assess its audit requirements based on the Indiana Code IC 5-11-1-9. This report must be filed within thirty days following the end of the entity's fiscal year.

Who needs to file the Entity Annual Report (Form E-1)?

Any entity, including corporations, partnerships, associations, and not-for-profit organizations, operating within Indiana and receiving government funds is required to file this report. It is essential for the determination of the entity's audit requirements by the State Board of Accounts.

What information is required on Form E-1?

The form requires detailed information about the entity such as the legal name, type of organization, federal ID number, business phone number, and contact information of the operating officer. It also demands a financial summary of the government funds received and disbursed within the year, plus the entity's total disbursements. Further details on the government funds received must be specified, and the entity is asked about its foundation, purpose, governing structure, and any previous audits by an Independent Public Accountant (IPA).

What is the deadline for filing the Entity Annual Report in Indiana?

The deadline for filing the Entity Annual Report (Form E-1) with the Indiana State Board of Accounts is within thirty days after the close of the entity's fiscal year end. It's crucial to adhere to this timeframe to ensure compliance and avoid any potential issues regarding audit requirements.

Can the Entity Annual Report be submitted electronically?

The document does not specify the acceptable methods for submission directly. However, entities interested in submitting the Entity Annual Report should contact the State Board of Accounts directly, either through their website at www.in.gov/sboa or by phone at (317) 232-2513, to inquire about current submission methods, which may include electronic filing.

What happens if an entity fails to file Form E-1 on time?

If an entity does not submit Form E-1 within the designated period, it may face challenges with the State Board of Accounts regarding its financial accountability and audit requirements. Entities are encouraged to file on time to ensure their operations remain in good standing and to avoid any inconvenience or potential scrutiny.

Is assistance available for completing the Entity Annual Report?

Yes, assistance for completing Form E-1 is available. Detailed instructions are attached to the form itself. Additionally, entities can seek help or clarification from the State Board of Accounts by reaching out via their contact information provided on the form. They offer guidance through their website or direct communication over the phone.

Does filing the Entity Annual Report replace the need for an independent audit?

No, filing Form E-1 does not replace the need for an independent audit. The purpose of this report is to help determine an entity's audit requirements. Based on the information provided in Form E-1, an entity may still be required to undergo an audit by an Independent Public Accountant, depending on specific criteria set by the Indiana State Board of Accounts.

What is the significance of the audit determination on Form E-1?

The audit determination section on Form E-1 indicates whether the State Board of Accounts has decided that a complete audit is required for the entity, or if the audit requirement has been waived for the reported fiscal year. This decision is influenced by the financial data and other information provided in the report.

Where can I find more information about the Entity Annual Report and other requirements?

For more information about the Entity Annual Report (Form E-1) and other related requirements, visit the Indiana State Board of Accounts website at www.in.gov/sboa. Here, entities can access resources, guidance documents, and contact information for further assistance. Additionally, contacting the Board directly through phone or electronic communication is encouraged for specific queries or concerns.

Filling out the Entity Annual Report for Indiana can be a daunting task for many, especially for those who are doing it for the first time. It's crucial to avoid common mistakes that can lead to the rejection of your report or additional scrutiny from the State Board of Accounts. Below are six mistakes commonly made when completing this form:

Not filing within the deadline: The Entity Annual Report must be filed within thirty (30) days of the close of your entity's fiscal year. Overlooking this deadline is a common mistake that can cause unnecessary complications.

Incorrectly reporting financial information: Errors in reporting the financial information, such as government funds received and disbursed during the year, can lead to significant discrepancies. Ensure that all amounts are accurately reported and that the calculations for percentages are correct.

Failure to indicate the basis of accounting: The form asks whether the financial information is reported on a cash or accrual basis. Not specifying the accounting method used can result in an incomplete filing and potential misunderstanding of financial data.

Omitting the operating officer’s signature: The certification section at the bottom of the form requires the signature of the operating officer, title, printed name, and date signed. An unsigned form can be considered invalid.

Not attaching additional sheets when necessary: The section detailing government funds received during the year may require additional sheets for a complete account. Failure to attach these can lead to incomplete reporting of received government funds.

Providing inaccurate or incomplete legal status and type of organization: The form distinguishes between different legal statuses and types of organizations (e.g., corporation, partnership, individual). Providing incorrect information here can affect the accuracy of your report and the audit requirements placed on your entity.

It's also important to double-check all sections of the form for completeness and accuracy, including basic information like the legal name, federal ID number, and business address. Attention to detail can save a lot of time and trouble in the long run.

Here are some tips to avoid these mistakes:

By steering clear of these common pitfalls, you can streamline the filing process and ensure your Entity Annual Report in Indiana is completed accurately and efficiently. Always remember, when in doubt, consult with a professional who can provide guidance tailored to your specific situation.

Filing the Entity Annual Report in Indiana is a critical task for businesses, ensuring compliance and transparency in their operations. However, this document is just a part of a suite of paperwork needed throughout the year for maintaining good standing, regulatory compliance, and operational efficiency. Here are other commonly used forms and documents that often accompany the Entity Annual Report:

Together, these documents form a comprehensive framework supporting the operational, financial, and legal aspects of a business. By ensuring these documents are accurately maintained and timely filed, businesses can avoid legal pitfalls, maintain financial health, and foster trust amongst stakeholders. It's not just about meeting requirements; it's about laying a solid foundation for growth and success.

The Entity Annual Report Indiana form is similar to several other documents required by different government agencies for organizational oversight and accountability. These similarities help streamline the reporting process for entities and ensure that regulatory requirements are met efficiently.

One document similar to the Entity Annual Report Indiana form is the IRS Form 990, which is required for tax-exempt organizations. Both forms seek detailed information about an organization's financial activities, including revenues and expenditures, to assess accountability and the proper use of funds. However, the IRS Form 990 includes more detailed breakdowns of expenses and revenue sources, aligning with its purpose to ensure tax compliance and public transparency for nonprofit organizations.

Another document that shares similarities is the Uniform Business Report filed with state corporations divisions. Like the Entity Annual Report, this report collects basic information about the company, such as legal name, address, and type of organization. Both reports serve to confirm that an entity is in good standing and meets the statutory requirements for operating within the state. The key difference lies in the depth of financial reporting, with the Entity Annual Report requiring more detailed financial information, particularly regarding government funds.

Additionally, the Entity Annual Report resembles financial statements provided to Boards of Directors. These statements typically include a balance sheet, income statement, and cash flow statement. Both sets of documents outline the financial health of an organization, detailing income, expenses, and the specifics of financial activities. The main distinction is the audience; while financial statements are intended for internal review and decision-making, the Entity Annual Report serves as a regulatory compliance tool for external oversight bodies.

Filling out the Entity Annual Report for Indiana requires attention to detail and an understanding of both your entity's financial and organizational operations. To ensure accuracy and compliance, here are some guidelines on what you should and shouldn't do when completing this form.

Do:File the report within 30 days of the close of your entity's fiscal year end. Timing is crucial to remain in compliance and avoid penalties.

Review the instructions for completing Form E-1 carefully before you start filling out the form. This step will help ensure that you understand all requirements and provide accurate information.

Ensure all financial information is reported accurately, whether on a cash or accrual basis, as specified in the form. Accurate financial reporting is essential for a clear audit trail.

Use the legal name of your entity and the correct Federal ID No. when filling out the form. Consistency in how your entity is identified is important for legal and record-keeping purposes.

Include thorough details of government funds received, following the format requested on Page 2 of the form. Precise reporting of these funds is critical for audit requirements.

Certify that the data contained in the report is accurate to the best of your knowledge. The signature of the operating officer or an authorized signatory is required for certification.

Check all completed information for accuracy and completeness before submitting the report. This final review can help catch and correct any errors.

Forget to list the government funds received during the year by agency, address, program title, and amount received. Leaving out any of these details can lead to incomplete reporting.

Overlook the need to attach additional sheets if the space provided is not sufficient. It’s important to provide a complete financial picture.

Ignore the legal status and type of organization sections on the form. Proper classification is critical for state considerations and audit determinations.

Misstate the percent of government funds disbursed to entity's total disbursements. This calculation is essential for understanding the scope of governmental influence on your entity’s finances.

Submit the report without the signature and title of the operating officer or equivalent. The report needs this certification to be considered valid.

Assume the filing is complete without double-checking that all required sections are filled out. An incomplete form could result in processing delays or the need to resubmit.

Use inaccurate or outdated information. The data you provide must reflect the most recent fiscal year to ensure compliance and accurate audit determinations.

When discussing the Entity Annual Report in Indiana, it’s crucial to clear up some common misunderstandings. Misconceptions can lead to filing errors, missed deadlines, and unnecessary stress for business owners. Below are six common misconceptions about the Entity Annual Report in Indiana:

Addressing these misconceptions can help ensure that your entity remains in compliance and avoids any potential issues with the State Board of Accounts in Indiana.

Completing the Entity Annual Report in Indiana is crucial for organizations to ensure compliance with the State Board of Accounts. This process should be approached with diligence to avoid any potential issues. Here are five key takeaways to understand when filling out and using the Entity Annual Report form:

In completing the Entity Annual Report for Indiana, accuracy, completeness, and timeliness are paramount. Businesses must provide detailed financial data and specific information about their organization's structure and operations. By adhering to these requirements, entities ensure they meet their compliance obligations and effectively manage their audit requirements.

What Is a Financial Declaration - This form plays a vital role in child support considerations, ensuring decisions are based on accurate financial representations of both parents.

Indiana Otp 901 - Section for the signature of the taxpayer or authorized agent, indicating agreement with the submitted details.