Indiana St 103Dr Form in PDF

Indiana St 103Dr Form in PDF

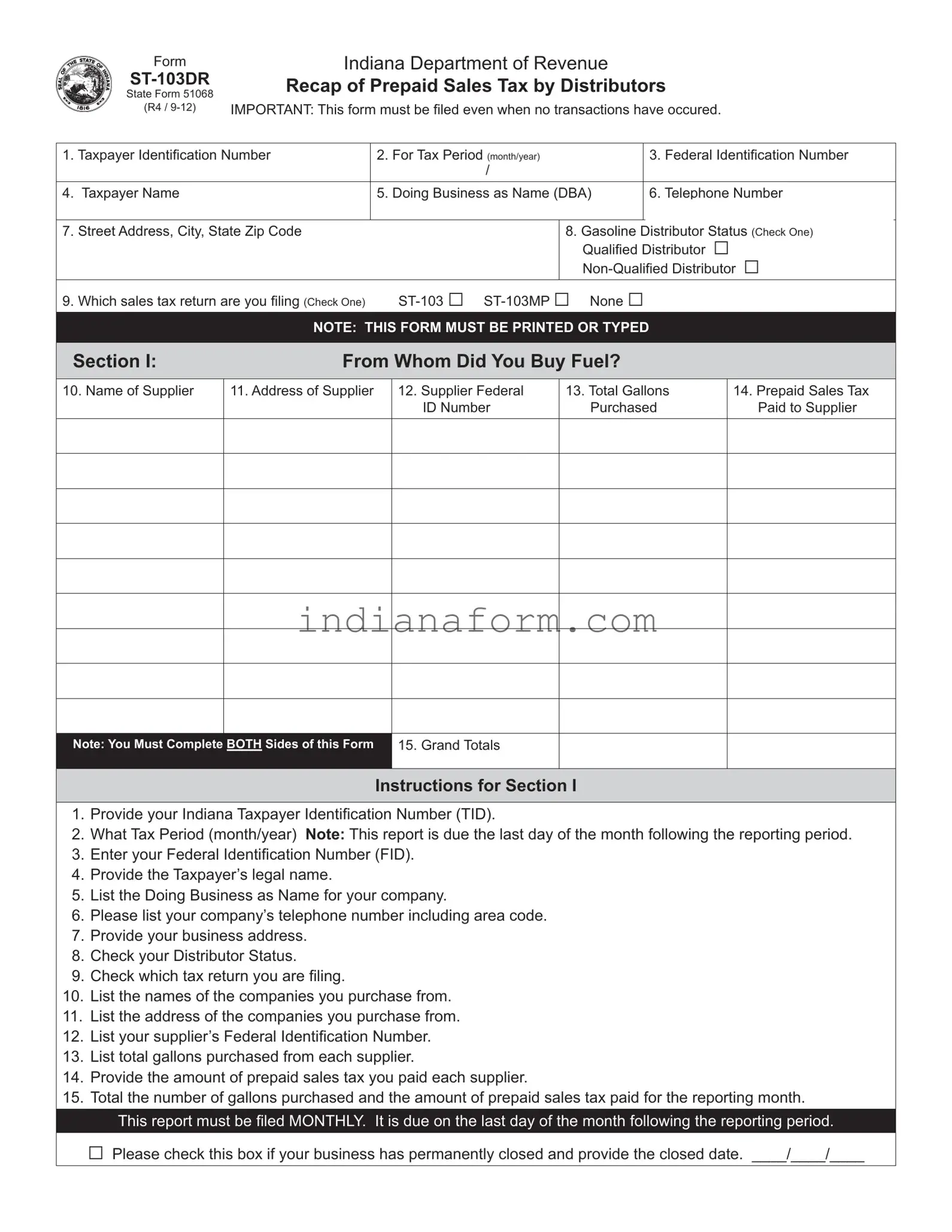

The Indiana Department of Revenue requires gasoline distributors to file the ST-103DR, officially known as the Recap of Prepaid Sales Tax by Distribitors form. This crucial document serves multiple functions, primarily facilitating accurate reporting and payment of prepaid sales taxes on gasoline distribution. Distributors must submit this form every month, even in cases where no transactions occur, ensuring consistent and transparent tracking of both purchase and sales activities within the state of Indiana. The form thoroughly covers the identification of the taxpayer, including the business's legal and DBA (Doing Business as) names, contact information, and tax identification numbers, both state and federal. It distinguishes between qualified and non-qualified distributor statuses and indicates the specific sales tax return being filed. Detailing purchases and sales, it requires information about fuel suppliers and customers, including names, addresses, Federal Identification Numbers, total gallons traded, and the amount of prepaid sales tax involved in these transactions. This meticulous documentation is essential for maintaining compliance with state taxation regulations, making it an indispensable tool for both the state and the businesses it governs. The form culminates in a declaration of the report's accuracy, under penalty of perjury, solidifying the filer's commitment to truthful reporting. The ST-103DR not only aids in the direct collection of taxes but also plays a significant role in the broader context of regulatory oversight and market integrity in the fuel distribution sector.

|

Form |

|

Indiana Department of Revenue |

|

|||

|

Recap of Prepaid Sales Tax by Distributors |

||||||

|

State Form 51068 |

||||||

|

|

|

|

|

|

|

|

|

(R4 / |

IMPORTANT: This form must be fi led even when no transactions have occured. |

|||||

|

|

|

|

|

|

||

1. Taxpayer Identifi cation Number |

|

2. For Tax Period (month/year) |

|

3. Federal Identification Number |

|||

|

|

|

|

/ |

|

|

|

|

|

|

|

|

|

|

|

4. |

Taxpayer Name |

|

|

5. Doing Business as Name (DBA) |

|

6. Telephone Number |

|

|

|

|

|

|

|

||

7. |

Street Address, City, State Zip Code |

|

|

8. Gasoline Distributor Status (Check One) |

|||

|

|

|

|

|

Qualifi ed Distributor □ |

||

|

|

|

|

|

|||

9. |

Which sales tax return are you filing (Check One) |

|

|||||

|

|

|

NOTE: THIS FORM MUST BE PRINTED OR TYPED |

|

|||

|

|

|

|

||||

Section I: |

|

From Whom Did You Buy Fuel? |

|

||||

10. Name of Supplier

11. Address of Supplier

12.Supplier Federal ID Number

13.Total Gallons Purchased

14.Prepaid Sales Tax Paid to Supplier

Note: You Must Complete BOTH Sides of this Form

15. Grand Totals

Instructions for Section I

1.Provide your Indiana Taxpayer Identifi cation Number (TID).

2.What Tax Period (month/year) Note: This report is due the last day of the month following the reporting period.

3.Enter your Federal Identifi cation Number (FID).

4.Provide the Taxpayer’s legal name.

5.List the Doing Business as Name for your company.

6.Please list your company’s telephone number including area code.

7.Provide your business address.

8.Check your Distributor Status.

9.Check which tax return you are filing.

10.List the names of the companies you purchase from.

11.List the address of the companies you purchase from.

12.List your supplier’s Federal Identification Number.

13.List total gallons purchased from each supplier.

14.Provide the amount of prepaid sales tax you paid each supplier.

15.Total the number of gallons purchased and the amount of prepaid sales tax paid for the reporting month.

This report must be fi led MONTHLY. It is due on the last day of the month following the reporting period.

□Please check this box if your business has permanently closed and provide the closed date. ____/____/____

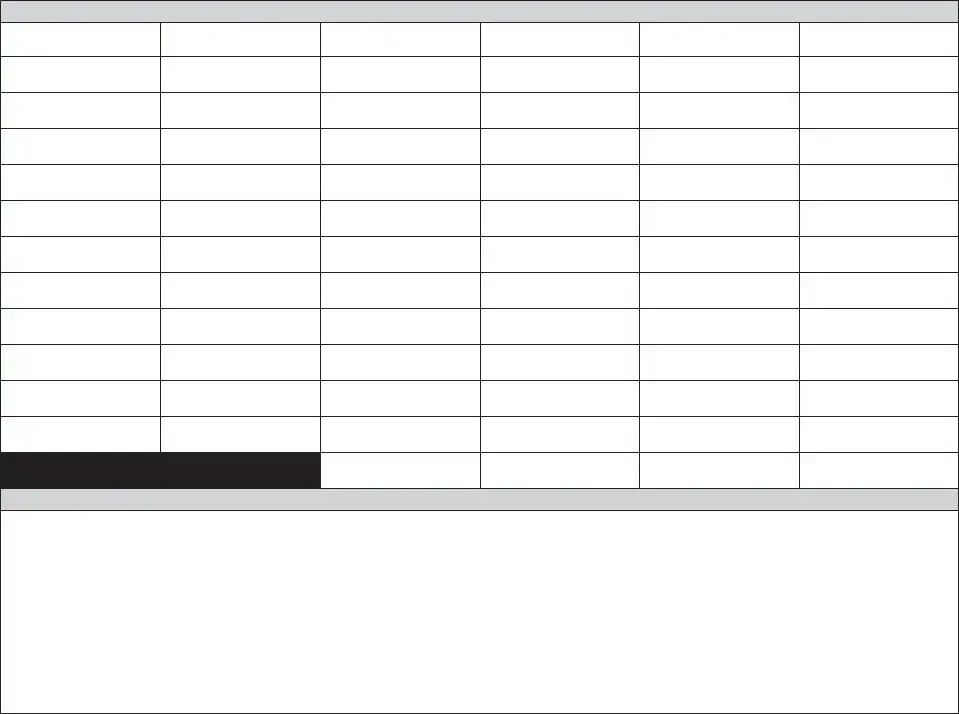

SECTION II |

To Whom Did You Sell Fuel? |

16. Customer’s Name

17. Customer’s Address

18.Customer’s Federal ID Number

19. Total Gallons Sold

20. Exempt Gallons Sold

21. Prepaid RST Collected

All Gallons EXEMPTED and TAXED must be shown

22. Total

Instructions for Section II

16.List your Customer’s Name. (Attach additional sheets if necessary).

17.List your Customer’s Address.

18.List your Customer’s Federal ID Number.

19.List the total gallons of gasoline sold for this month to each customer.

20.List the total tax exempt gallons sold to each customer.

21.List the total amount of Prepaid Sales Tax collected for this month from each customer.

22.Total the amounts of all columns and give the total gallonage and amount collected here.

I declare, under penalties of perjury that this is a true, correct and complete report.

Mail to: Indiana Department of Revenue Excise Tax

P.O. Box 6114 Indianapolis, IN

______________________________________________ |

_____________________________________________ |

__________________________ |

________________ |

Printed Name |

Authorized Signature |

Title |

Date |

| Fact | Detail |

|---|---|

| Purpose | Recap of Prepaid Sales Tax by Distributors |

| Governing Law | Indiana State Tax Law |

| Form Number | ST-103DR |

| State Form Number | 51068 (R4 / 9-12) |

| Filing Requirement | Must be filed monthly, even if no transactions occurred |

| Due Date | Last day of the month following the reporting period |

| Sections Included | Two main sections: From Whom Did You Buy Fuel? (I) and To Whom Did You Sell Fuel? (II) |

After wrapping up a report or making sales, managing your taxes accurately is crucial. Filling out the Indiana ST-103DR form is an important step that keeps you compliant with state tax laws. This form helps you report your prepaid sales tax activities as a distributor. Remember, this document is necessary even if there were no transactions in the reporting period. The steps below guide you through filling out each section of the form properly, ensuring you stay on top of your business responsibilities.

Once you've completed the form, mail it to the Indiana Department of Revenue at the address provided. Staying diligent in your tax reporting not only keeps your business in good legal standing but also helps streamline your financial operations.

What is the purpose of the Indiana ST-103DR form?

The Indiana ST-103DR form, also known as the Recap of Prepaid Sales Tax by Distributors form, is utilized by distributors to report and recapitulate the total gallons of fuel purchased and sold, along with the amount of prepaid sales tax paid to suppliers and collected from customers. It is a mandatory filing to ensure compliance with the state's tax regulations.

Who is required to file the ST-103DR form?

Any distributor engaged in the business of selling fuel within the state of Indiana is required to file the ST-103DR form. This includes both qualified and non-qualified gasoline distributors as identified under state tax guidelines.

When is the ST-103DR form due?

The ST-103DR form must be filed monthly. The due date for submission is the last day of the month following the reporting period. For instance, for sales in January, the form is due by the end of February.

Are there any penalties for filing the ST-103DR form late?

Yes, distributors who fail to file the ST-103DR form by the due date may be subject to penalties and interest as determined by the Indiana Department of Revenue. These can include charges for late filing and late payment, which accrue over time until the form is submitted and the due tax is paid.

What information is needed to complete the ST-103DR form?

To accurately complete the ST-103DR form, distributors must provide their Indiana Taxpayer Identification Number (TID), Federal Identification Number (FID), the tax period, taxpayer's legal name and DBA (Doing Business as Name), contact and business address details, their distributor status, and details of fuel transactions including purchases and sales with corresponding prepaid tax amounts.

Can the ST-103DR form be filed if there were no transactions during the reporting period?

Yes, the Indiana Department of Revenue requires that the ST-103DR form be filed even if the distributor had no transactions during the reporting period. This ensures ongoing compliance and maintains accurate records with the tax authority.

What should I do if my business permanently closes?

If your business permanently closes, you should indicate this status on the ST-103DR form by checking the appropriate box and providing the date of closure. This information is crucial for the Indiana Department of Revenue to update their records accordingly.

Where do I mail the completed ST-103DR form?

The completed ST-103DR form should be mailed to the Indiana Department of Revenue Excise Tax, P.O. Box 6114, Indianapolis, IN 46206-6114. It is advisable to keep a copy of the form for your records.

How can I verify that my ST-103DR form was received and processed?

To verify the receipt and processing of your ST-103DR form, you can contact the Indiana Department of Revenue Excise Tax Division at (317) 615-2552. It is recommended to wait a few weeks after mailing your form before making an inquiry.

What do I do if I make a mistake on the ST-103DR form?

If you discover an error on the ST-103DR form after submission, you should contact the Indiana Department of Revenue for guidance on how to submit a corrected form. It's important to address any inaccuracies as soon as possible to ensure compliance and avoid potential penalties.

When filling out the Indiana ST-103DR form, which is essential for distributors to report prepaid sales tax, people sometimes make errors that can complicate the process. Recognizing and avoiding these mistakes can save time and ensure compliance with Indiana tax regulations.

One of the most common mistakes is not providing the Indiana Taxpayer Identification Number (TID) accurately. This number is crucial for the Department of Revenue to identify your business and process the form properly. Ensure that the number is entered correctly and matches the number registered with the state.

Another frequent error is failing to report the correct Tax Period (month/year). This detail is critical because it informs the department of the specific time frame for the reported transactions. Mixing up dates or providing a vague period can lead to confusion and potentially result in late fees or penalties for filing incorrect information.

Often, individuals neglect to check the appropriate box under the Gasoline Distributor Status section. Whether you are a Qualified Distributor or a Non-Qualified Distributor affects how the prepaid sales tax is handled. Mistakenly identifying your distributor status can lead to inaccuracies in how your taxes are calculated and processed.

Let’s not overlook the documentation required for Section II, including accurately listing each customer’s Federal ID Number and the total gallons sold. It is easy to overlook details when dealing with multiple transactions, but each piece of information contributes to the total sales tax owed or to be reimbursed. Remember, all gallons, whether exempt or taxed, must be accounted for, which people sometimes miss.

In sum, careful attention to detail can prevent these common mistakes. Always double-check the information before submission to ensure compliance and accuracy in your tax reporting.

When dealing with the complexities of filing taxes in Indiana, especially for distributors, the Indiana ST-103DR form plays a crucial role in reporting prepaid sales tax. However, this form doesn't stand alone in the landscape of tax documentation and compliance. Distributors often find themselves needing to fill out and submit additional forms and documents alongside the ST-103DR, each fulfilling a unique purpose in ensuring that all aspects of tax reporting are accurately covered.

Comprehending the purpose and requirement of each form illuminates the nuanced process of tax compliance in Indiana. For distributors, the journey begins with the ST-103DR but invariably involves a host of other documents, each serving to ensure comprehensive and accurate tax reporting. It's this interconnected web of forms and the details therein that uphold the integrity of the state's tax system, ultimately facilitating a smoother operational flow for businesses engrossed in the distribution of taxable goods.

The Indiana ST 103DR form, focused on the recap of prepaid sales tax by distributors, shares similarities with several other tax reporting documents, each designed to capture specific transactional details for tax purposes. These forms not only fulfill regulatory requirements but also aid businesses in maintaining accurate records of their financial activities. Understanding these similarities provides valuable insights into the intricacies of tax documentation and compliance.

The Indiana ST-103 Sales and Use Tax Voucher is one such document that bears resemblance to the ST 103DR form. Like the ST 103DR, the ST-103 form is used by businesses to report and pay collected sales tax to the state. Both forms require the taxpayer's identification information and specific period details for which the tax is being reported. However, the ST-103 is broader, encompassing sales tax collected directly from consumers, whereas the ST 103DR is specific to prepaid sales tax on fuel distributions. The common ground lies in their purpose to ensure tax compliance and accurate reporting of taxable transactions to the Indiana Department of Revenue.

The Form ST-103MP, specifically designed for marketplace facilitators, is another document that shares functionalities with the ST 103DR form. This form enables marketplace facilitators to report sales tax collected on behalf of sellers using their platform. Similar to both the ST-103 and ST 103DR forms, the ST-103MP requires detailed identification and transactional information from the filer, including the tax period and the amount of tax collected and remitted. While the ST 103DR focuses on fuel distributors, and the ST-103 encompasses a broader array of businesses, the ST-103MP zeroes in on the unique role of marketplace facilitators, creating a tailored approach to sales tax compliance.

In conclusion, while each form serves a distinct segment of the business and tax landscape, the Indiana ST 103DR, ST-103, and ST-103MP forms collectively ensure that entities, whether dealing in general consumer sales, fuel distribution, or marketplace facilitation, comply with Indiana’s sales tax laws. Their structured formats and required information fields streamline the tax reporting process, making it manageable for businesses to fulfill their tax obligations accurately and efficiently.

When filling out the Indiana ST-103DR form, it's important to keep in mind a few dos and don'ts to ensure the process is smooth and error-free. This form, crucial for those in the distribution sector, must be filled out correctly to comply with Indiana's Department of Revenue requirements. Here are key pointers to help you along:

Do:

Don't:

By following these guidelines, you can complete the Indiana ST-103DR form correctly and efficiently, ensuring compliance with state tax requirements and avoiding potential pitfalls.

When it comes to filling out the Indiana Department of Revenue ST-103DR, commonly known as the Recap of Prepaid Sales Tax by Distributors form, there are several misconceptions that can create confusion. Addressing these misunderstandings can simplify the process and ensure compliance with state requirements.

Misconception #1: The ST-103DR form is only required for months with sales transactions. Truth: Regardless of having transactions or not, distributors must file this form monthly.

Misconception #2: Only gasoline distributors need to file this form. Truth: While the form is predominantly used by gasoline distributors, it also applies to distributors dealing with other types of fuel under certain conditions.

Misconception #3: The form is due annually. Truth: This form must be filed monthly, specifically by the last day of the month following the reporting period.

Misconception #4: Electronic submissions are not allowed. Truth: The Indiana Department of Revenue accepts electronic filings, making submission more convenient and efficient.

Misconception #5: If my business closes, I don’t need to file this form. Truth: If a business permanently closes, it must indicate so on the form and provide the closure date. This final submission is crucial for proper record-keeping and to avoid penalties.

Misconception #6: Personal identification information is unnecessary when filing the ST-103DR. Truth: Distributors must provide both their Taxpayer Identification Number (TID) and Federal Identification Number (FID) to correctly process the form.

Misconception #7: Detailed transaction records are not required. Truth: The form requires detailed information, including the total gallons purchased or sold, the tax paid or collected, and identifying details of suppliers and customers to ensure transparency and accurate tax calculation.

Misconception #8: Section II of the form is optional. Truth: Both sections of the ST-103DR form are mandatory, providing a comprehensive report of prepaid sales tax on fuel distributed within Indiana.

Misconception #9: Only total gallons and total taxes need to be reported. Truth: Distributors must report not just total gallons and taxes but must also distinguish between taxed and exempt gallons, providing a clear and complete fiscal snapshot.

Understanding and addressing these misconceptions about the ST-103DR form can significantly reduce filing errors, ensure state compliance, and avoid potential penalties for distributors in Indiana.

Filling out the Indiana ST-103DR form correctly is crucial for distributors dealing with gasoline sales in Indiana. Here are six key takeaways to ensure you complete this form accurately and stay in compliance with state regulations.

Filling out the Indiana ST-103DR form might seem daunting at first glance, but understanding these key takeaways makes the process more manageable. Diligence, accuracy, and timely submission are your best practices when dealing with this essential aspect of your business’s operational compliance.

Dcs Forms - Provides parents, guardians, or custodians with contact information for the local Department of Child Services office.

Uc-1 - Navigating credits from previous quarters in UC-1 form submissions, aiding in accurate financial reporting.

Paternity Affidavit Indiana - Both biological and presumed fathers may use this form, provided all legal conditions for paternity acknowledgment are met according to Indiana law.