Indiana St 105 Form in PDF

Indiana St 105 Form in PDF

The Indiana ST-105 General Sales Tax Exemption Certificate plays a crucial role for registered retail merchants in Indiana as well as for businesses located outside the state but conducting transactions within Indiana. Crafted to cater to a variety of businesses, the form stipulates that only certain exemptions under the Indiana code are legitimate, explicitly excluding utility, vehicle, watercraft, or aircraft purchases. A pivotal requirement is the completion of all segments of the form to validate any claim for exemption from sales tax. Additionally, this document necessitates the provision of a specific identification number that validates the purchaser's eligibility. This might include an Indiana Department of Revenue issued Taxpayer Identification Number or an equivalent from another state if the business is not registered in Indiana. Furthermore, the form also details scenarios where alternate identifiers, such as a Federal Identification Number or Social Security Number, may suffice. This certificate not only aids in the regulation of tax exemption claims, strictly adhering to the stipulated Indiana Code 6-2.5, but also emphasizes the severe consequences of any misuse ranging from the retraction of tax exemption privileges to the imposition of fines or even criminal charges. Sellers are mandated to retain this certificate to substantiate any exempt sales, marking a critical document for both parties involved in the transaction.

Form |

Indiana Department of Revenue |

StateForm :19065 |

General SalesThx Exemption Certificate |

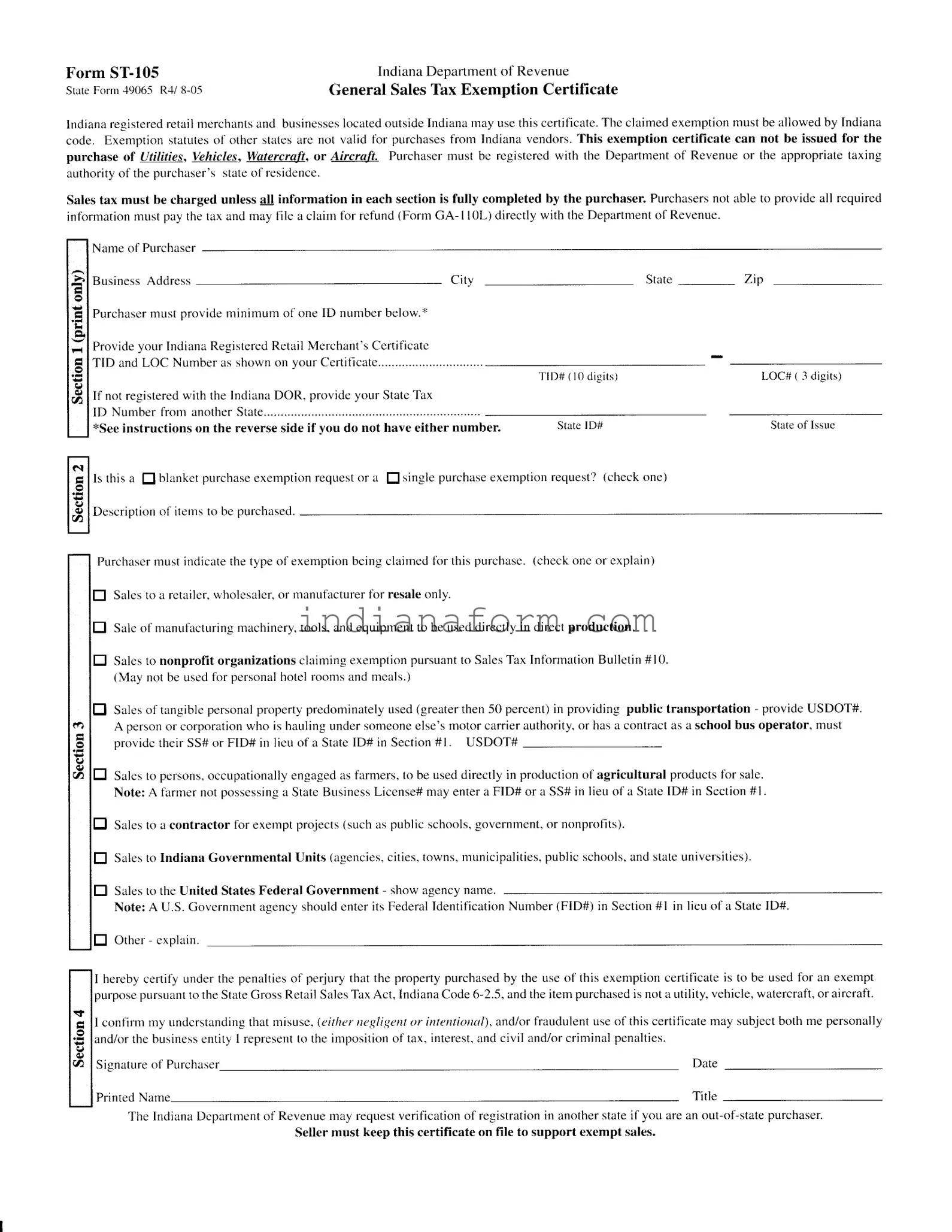

Indianaregisteredrelail merchantsand businesseslocatedoutsideIndianamay usethis certificate.The claimedexemptionmust be allowedby Indiana code. Exemption slatutesof other statesare not valid tbr purchasesfrom Indiana vendors.This exemption certilicate can not be issued for the purchase of lLili/iqg, Vehicles, Watercraft, or Ai/crafr. Pttrcha.sermust be registered with the Depafiment of Revenue or the appropriate taxing authorityofthe purchaser'sstateof residence.

Sales tax must be charged unless a!! information in each 6ection is fully completed by the purchaser. Purchasersnot able to provide all required informationmust pay the tax and may file a ctaim for refund(Form GA- I

Name of Purchaser

B u s i n e s s A d d r e s s |

C i t y |

P u r c h a s e rm u s t p r o v i d e m i n i m u m o f o n e I D n u n i b e r b e l c l w . t '

Provide your Indiana Registered Retail Merchant's Certificatc TID and LOC Number as shown on your Certificate .

If not registered with the Indiana DOR, provide your State Tax I D N u m b e r f r o m a n o t h e r S t a t e . . . . . .

*See instructions on the reverse side if vou do not have either number .

State _ |

Zip |

T I D # ( l 0 d i g i t s ) |

LOC# ( 3 digits) |

SrarelD# |

Stateof Issue |

HI s t h i s a I b l a n k e t p u r c h a s ee x e m p t i o n r e q u e s to r a I

D e s c r i p t i o no f i l e m s t o b e p u r c h a s e d .

s i n g l e p u r c h a s ee x e m p t i o n r e q u e s t ? ( c h e c k o n e )

Purchasermust indicatethe lype oI exemptionbeing claimedfor this purchase.(checkone or explain)

E

E

E

E

Salesto a retailer,wholesaler,or manufacturerfor resaleonly.

Saleof manufactu ng machinery tools.andequipmentto be useddirectly in direct production.

Salesto nonprofft organizations claimingexemptionpursuantto SalesTax lnformationBullelin #10. (May not be usedfor personalhotel roomsand meals.)

Salesofrangible personalpropertypredominatelyused(greaterthen50 percent)in providing public transportation - provide USDOT#.

Apersonor corporalionwho is baulingundersomeoneelse'smotor carrierauthority,or hasa contractasa schoolbus operator, must providc their SS#or FID# in lieu of a StateID# in Section#1. USDOT# -

E

E

E

Salesto persons,occupationallyengagedasfamers, to be useddirectly in productionof agricultural productsfor sale. Note: A farmernot possessinga StateBusinessLicense#may entera FID# or a SS# in lieu of a StateID# in Section#1.

Salesto a contractor for exemptprojects(suchaspublic $chools,or nonprofits). Sovemment,

Salesto Indiana Governmental Units (agencies,cilies,towns.municipalities,public schools,and slateuniversities).

El

Salesto the United States Federal Government - show agency name .

Note: A U . S . Government asencv should enter its Federal Identification Number (FID#) in Section #1 in lieu of a State ID# .

E O t h e r - e x p l a i n .

Iherebycerlify underthe penaltiesof perjury that lhe propeny purchasedby the useof this exemptioncertificateis to be usedfor an exempt purposepursuanlto theStateCrossRetailSalesTaxAct,

Iconfirm my undeBtandingthat misuse,(?ifrer egligentor intentioral), and/orfraudulentuseofthis certificatemay subjectboth me personally and/orthe businessentity I represenlto the impositionoftax, interest,and civil and/orcriminal penalties.

Signature of Purchaser |

Date |

Printed Name |

Title |

The Indiana Dcpartntent of Revenue may request verification of registration in another state if you are an out - of - state purchaser .

Seller must keep this certificate on file to support exempt sales.

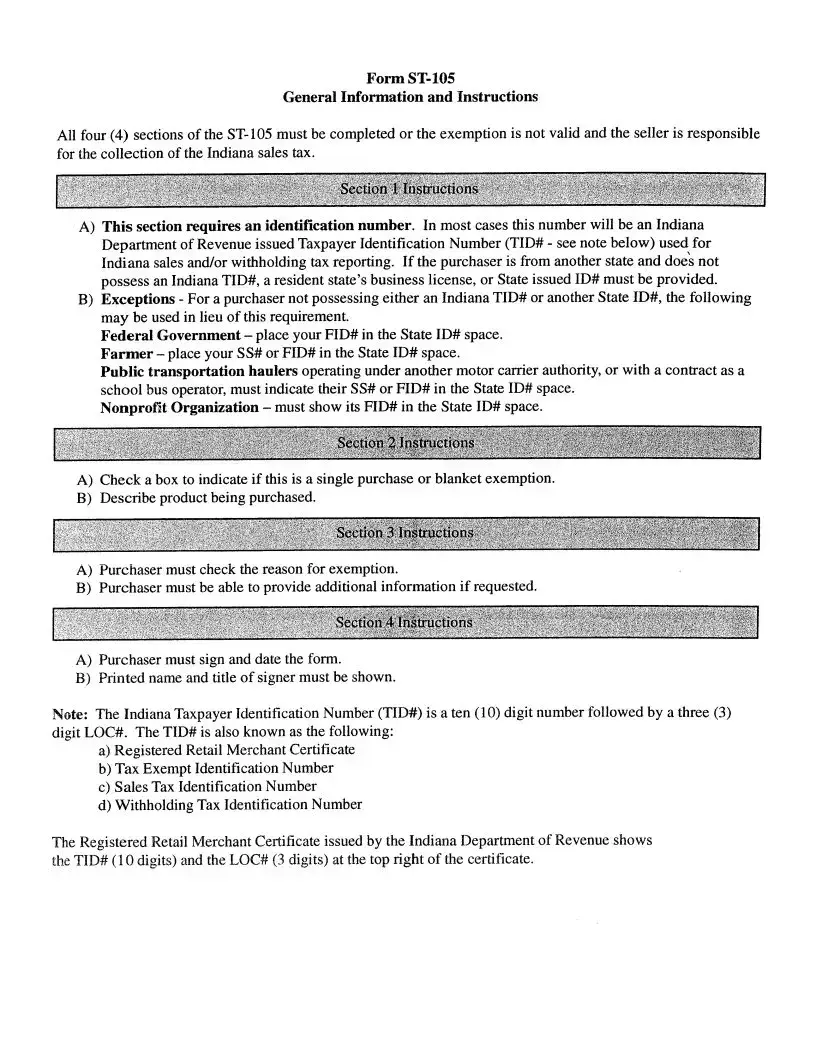

GeneralInfonnation and Instructions

All four (4) sectionsof

A)This sectionrequires an identification number. In mostcasesthis numberwill be anIndiana DeparunentofRevenueissuedTaxpayerldentificationNumber(TID# - seenotebelow) usedfor Indianasalesand/orwithholdingtax reporting. If the purchaseris from anotherstateanddoei not possessanIndianaTID#, a residentstate'sbusinesslicense,or StateissuedID# mustbeprovided.

B)Exceptions- For a purchasernot possessingeitheranIndianaTID# or anotherStateID#, thefollowing

may beusedin lieu of thisrequirement. tr'ederalGovernment- placeyourFID# in theStateID# space. Farmer - placeyour SS#or FID# in theStateID# space.

Public transportation haulersoperatingunderanothermotor carrierauthority,or witb a contractasa

schoolbusoperator,mustindicatetheir SS#or FID# in theStateID# space. Nonprolit Organization- mustshowits FID# in the StateID# space.

A)Check a box to indicateif this is a singlepurchaseor blanketexemption.

B)Describeproductbeingpurchased.

A)Purchasermustcheckthereasonfor exemption.

B)Purchasermustbe ableto provide additionalinformation if requested.

A)Purchasermust sign and date the form.

B)Printednameandtitle of signermustbe shown.

Note: The Indiana TlrxpayerIdentification Number (TID#) is a ten (10) digit number followed by a thtee (3) digit LOC#. The TID# is alsoknown asthe following:

a)RegisteredRetail Merchant Certificat€

b)Tax Exempt Identification Number

c)SalesTax Identification Number

d)Withholding Tax Identification Number

The RegisteredRetailMerchantCertificateissuedby the IndianaDepartrnentofRevenueshows the TID# ( I 0 digits) and the LOC# (3 digits) at the top right of the certificate'

| Fact | Detail |

|---|---|

| 1. Purpose | The Form ST-105 is used to claim sales tax exemption by Indiana registered retail merchants and businesses located outside Indiana. |

| 2. Exclusions | Cannot be used for purchases of utilities, vehicles, watercraft, or aircraft. |

| 3. Validity | Exemptions from other states are not valid; must be based on Indiana Code. |

| 4. Completion Requirement | All sections must be fully completed for the exemption to be valid. If not fully completed, sales tax must be charged. |

| 5. Identification Numbers | Purchasers must provide either an Indiana Department of Revenue issued Taxpayer Identification Number (TID) and LOC Number or a State Tax ID Number from another state. |

| 6. Verification | The Indiana Department of Revenue may request verification of registration from out-of-state purchasers. |

| 7. Record Keeping | Sellers must keep the completed certificate on file to support exempt sales. |

| 8. Governing Law | Indiana Code 6-2.5 |

Filling out the Indiana ST-105 form is a crucial task for Indiana-registered retail merchants and businesses located outside Indiana when they need to claim tax exemption for certain purchases. This document needs to be accurately completed to ensure compliance with Indiana Code, allowing for tax exemptions under valid statutes. It is imperative that every section of the form is filled out thoroughly, as any incomplete information could result in the denial of the tax exemption claim and make the seller responsible for the collection of Indiana sales tax. Following the below steps will guide you through the process of filling out the form correctly.

It is essential for both the purchaser and the seller to understand that maintaining accurate records and compliance with the Indiana Department of Revenue's requirements is crucial. The seller is obliged to keep this certificate on file to support exempt sales. Misuse or fraudulent use of this certificate can lead to serious consequences, including tax liability, interest, and possible civil or criminal penalties. Therefore, ensuring that the ST-105 form is properly filled out and submitted is a shared responsibility that facilitates tax compliance and supports the integrity of business operations in Indiana.

What is the Form ST-105 and who uses it?

The Form ST-105 is the General Sales Tax Exemption Certificate used in Indiana. It is employed by Indiana-registered retail merchants and businesses located outside Indiana. This form allows entities to make tax-exempt purchases provided the exemption is allowed under Indiana code. Note that the claimed exemption must adhere to Indiana’s stipulations, as exemptions from other states are not valid for purchases from Indiana vendors.

Can the Form ST-105 be used for all purchases?

No, the Form ST-105 cannot be issued for the purchase of utilities, vehicles, watercraft, or aircraft. These types of purchases are excluded from the exemptions covered by this certificate.

What information is required to complete the Form ST-105?

To properly complete the Form ST-105, all sections of the form must be filled out thoroughly. This includes providing a qualified identification number. If the purchaser is registered with the Indiana Department of Revenue (DOR), they will provide their Indiana Registered Retail Merchant's Certificate Number (TID and LOC Number). If not registered in Indiana, the purchaser should provide their State Tax ID Number from another state. Details about the purchase, including whether it is a single or blanket purchase and the specific type of exemption being claimed, are also required.

What happens if I can't provide all the required information on the ST-105?

If a purchaser cannot provide all the necessary information on the Form ST-105, sales tax must be charged on the purchase. However, the purchaser may then file a claim for a refund (using Form GA-110L) directly with the Indiana Department of Revenue.

Are there exceptions to the identification number requirement?

Yes, in cases where a purchaser does not possess either an Indiana TID# or another State ID#, alternate identifiers may be used. Federal Government buyers can use their FID#; farmers have the option of providing SS# or FID#; public transportation haulers operating under another’s authority, or as a school bus operator, can also use SS# or FID#; and non-profit organizations should provide their FID# in the appropriate section.

How does one distinguish between a single purchase and a blanket exemption on the ST-105?

On the Form ST-105, the purchaser must check the appropriate box to indicate whether the exemption request is for a single purchase or is a blanket exemption. A single purchase exemption relates to a one-time purchase, while a blanket exemption covers multiple purchases over time.

What types of exemptions can be claimed using the ST-105?

The ST-105 allows for several types of tax exemptions. These include purchases by retailers, wholesalers, or manufacturers for resale; purchases of manufacturing machinery and equipment; purchases by non-profit organizations; items used predominantly in public transportation; agricultural production items by farmers; purchases by contractors for exempt projects; purchases by Indiana governmental units or the United States Federal Government; among other specific exemptions provided under Indiana law.

What is the penalty for misuse of the Form ST-105?

Misuse, whether negligent or intentional, or fraudulent use of the Form ST-105, may subject the purchaser and/or the business entity represented to the imposition of tax, interest, and possibly civil and/or criminal penalties under the penalties of perjury clause of the Indiana Code 6-2.5.

Is it necessary for the seller to keep a copy of the completed ST-105?

Yes, the seller must keep the completed Form ST-105 on file to support exempt sales. This documentation serves as evidence of due diligence in complying with Indiana sales tax laws and is crucial for audit purposes.

Filling out tax forms can be a bit like navigating a maze, and the Indiana ST-105 form is no exception. This form, essential for claiming sales tax exemptions in Indiana, comes with its own unique set of challenges. People often make several mistakes when completing this form, which can lead to the denial of their exemption claim. Let's delve into some of the common errors to help ensure your journey through this paperwork jungle is a bit smoother.

First and foremost, a crucial error is not fully completing all required sections. The form clearly states that all four sections must be completed for the exemption to be valid. Yet, it's not uncommon for individuals to overlook or partially fill out sections, especially if they're in a rush or are unfamiliar with the form's requirements.

Avoiding these pitfalls is key to successfully navigating the ST-105 form. Always double-check your details, ensure you understand the requirements, and when in doubt, consult with a tax professional. This way, you can claim your exemptions with confidence, knowing you've accurately navigated the intricacies of the form.

When utilizing the Indiana ST-105 General Sales Tax Exemption Certificate, various other forms and documents often accompany or are relevant to the process. Understanding these additional documents can streamline transactions and ensure compliance with Indiana's tax regulations.

Understanding and properly utilizing these forms and documents, in conjunction with the ST-105, facilitates efficient handling of exempt transactions. This comprehensive approach ensures both compliance with Indiana tax laws and maximizes operational efficiency for businesses and organizations.

The Indiana ST-105 form, issued by the Indiana Department of Revenue, is a General Sales Tax Exemption Certificate designed to allow qualifying retailers and businesses to purchase goods without paying sales tax, provided these goods are for resale or meet other specific exemption criteria outlined by Indiana law. This form is notably similar to other state-specific sales tax exemption certificates, each serving a comparable purpose but under the guidelines of different state regulations. Understanding how the ST-105 form aligns with forms from other states sheds light on the broader context of sales tax exemption in the United States.

One document that bears resemblance to the Indiana ST-105 form is the New York State ST-120 Resale Certificate. Like the ST-105, the ST-120 allows retailers and certain other entities to purchase goods without paying state sales tax, assuming these goods are intended for resale or qualify under specific exceptions defined by New York state law. Both forms require the purchaser to provide detailed information about their business, including a state-issued taxpayer identification number or equivalent, and to specify the nature of the exemption being claimed. However, whereas the ST-105 is governed by Indiana's tax codes, the ST-120 operates under New York's distinct tax laws and regulations, reflecting the variance in tax policy from state to state.

Similarly, the California Resale Certificate (BOE-230), like Indiana's ST-105, serves the purpose of documenting a purchaser's intent to buy goods tax-free for the purpose of resale. Both documents necessitate that the purchaser be a registered merchant or hold a comparable certification within their respective state. They must accurately detail the type of business conducted and the specific use of the purchased goods that qualifies for tax exemption. While both the ST-105 and BOE-230 facilitate a similar end—purchasing for resale without bearing the immediate burden of sales tax—the criteria and specific instructions reflect the legislative nuances particular to California and Indiana, respectively.

Moreover, the Texas Sales and Use Tax Resale Certificate (Form 01-339) parallels the function of Indiana's ST-105 by allowing businesses to procure goods tax-free when those goods are intended for resale or for the creation of a taxable service. Both forms are critical for businesses to navigate the tax landscape efficiently, avoiding unnecessary taxation on purchases that are not final sales. Each form underscores the necessity for purchasers to explicitly state the reason for exemption, and like their counterparts, mandates the provision of a taxpayer identification number or equivalent certification. Yet, the content and structure of these forms are tailored to fit within the regulatory framework specific to Texas, showcasing the diversity in how states approach sales tax exemptions.

In essence, while the Indiana ST-105 form is unique to Indiana in its application and requirements, its counterparts across the United States share a common goal: facilitating tax-free purchases for qualifying transactions, particularly those involving resale. The differences among these forms illustrate the variability in state policies regarding sales tax exemptions, emphasizing the importance for businesses to understand and comply with the specific requirements of each state in which they operate.

When filling out the Indiana ST-105 form, it's important to pay attention to details to ensure the process goes smoothly and correctly. Here are some dos and don'ts to keep in mind:

Do:When discussing the Indiana ST-105 form, there are several misconceptions that warrant clarification. This document is crucial for businesses seeking sales tax exemptions on their purchases but is often misunderstood. Here’s a breakdown of the ten most common misconceptions.

Understanding the intricacies of the Indiana ST-105 form is crucial for businesses attempting to navigate the complexities of tax exemptions. Misconceptions can lead to costly errors. It’s essential for merchants and their advisers to grasp the scope, limitations, and requirements of this certification to ensure compliance and avoid penalties.

Uc-5a - It includes instructions for employers on how to properly report employee wages and personal information.

Indiana State Police Accident Reports - Allows for supplementary reports if initial information provided is deemed insufficient.