Indiana State 104 Form in PDF

Indiana State 104 Form in PDF

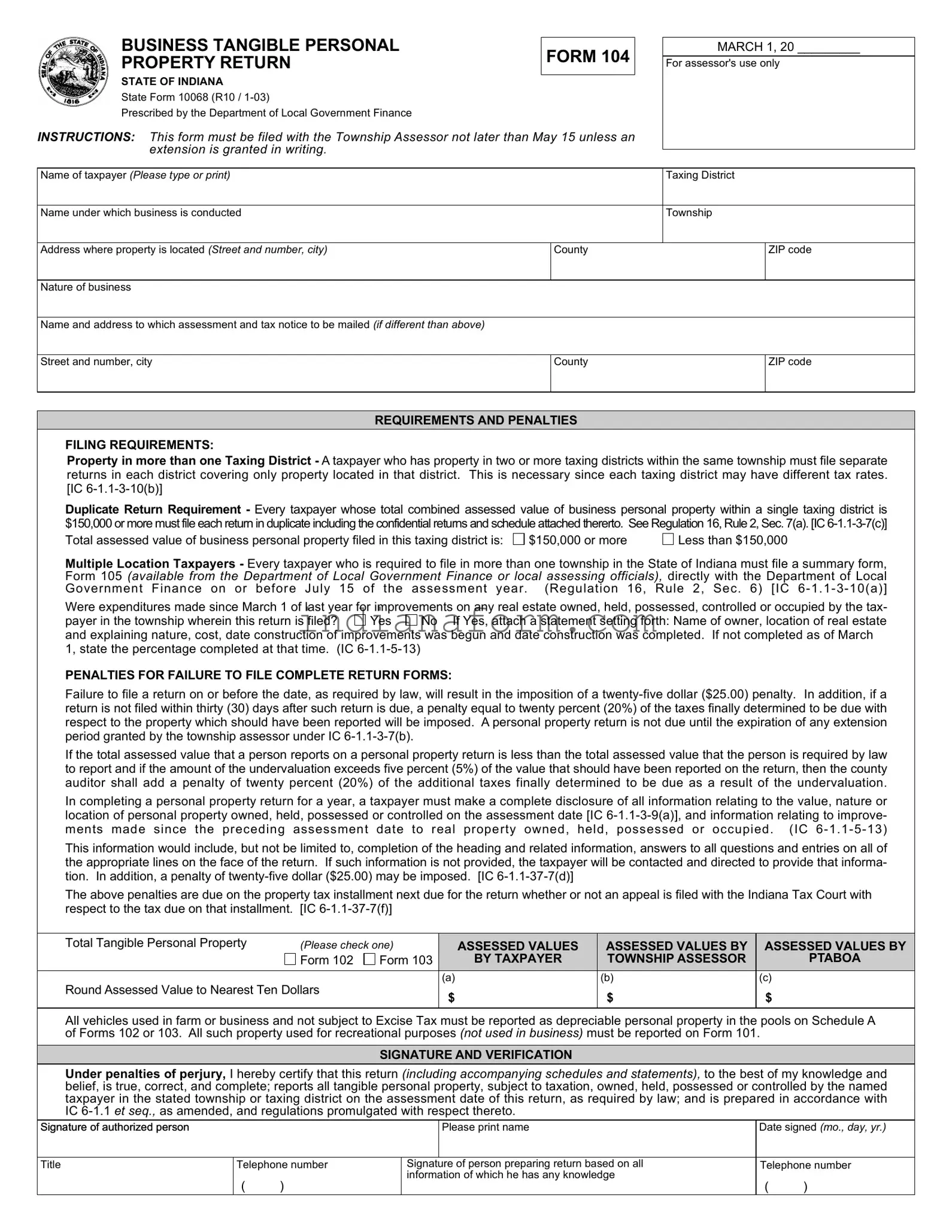

Understanding the nuances and obligations associated with the Indiana State 104 form is crucial for businesses maintaining tangible personal property within the state. Recognized formally as the "Business Tangible Personal Property Return," this document, mandated by the Department of Local Government Finance, plays a pivotal role in the assessment and taxation process of business-owned personal property. Deadline adherence is critical, with the form requiring submission to the Township Assessor by no later than May 15, unless a written extension is granted. It encompasses detailed declarations from taxpayers regarding the location, nature, and assessed value of their tangible personal assets within Indiana, distinguishing between properties across different taxing districts and specifically addressing multi-location taxpayers through supplemental forms. The form further mandates disclosure of any recent improvements on real estate related to the business, underscoring the necessity of thorough and accurate reporting. Penalties for non-compliance, incomplete returns, or undervaluation of reported property underscore the seriousness with which the state regards this obligation. Such penalties can include monetary fines or increased tax liabilities, highlighting the financial implications of misreporting or omission. The completion process also involves a certification of the return’s accuracy under the penalties of perjury, ensuring that all information presented is both comprehensive and truthful, as outlined within the broader regulatory framework of Indiana Code 6-1.1 et seq. and applicable regulations.

BUSINESS TANGIBLE PERSONAL |

FORM 104 |

|

PROPERTY RETURN |

||

|

||

|

|

STATE OF INDIANA

State Form 10068 (R10 /

Prescribed by the Department of Local Government Finance

INSTRUCTIONS: This form must be filed with the Township Assessor not later than May 15 unless an extension is granted in writing.

MARCH 1, 20 _________

For assessor's use only

Name of taxpayer (Please type or print) |

|

Taxing District |

|

|

|

|

|

Name under which business is conducted |

|

Township |

|

|

|

|

|

Address where property is located (Street and number, city) |

County |

|

ZIP code |

|

|

|

|

Nature of business |

|

|

|

|

|

|

|

Name and address to which assessment and tax notice to be mailed (if different than above) |

|

|

|

|

|

|

|

Street and number, city |

County |

|

ZIP code |

|

|

|

|

REQUIREMENTS AND PENALTIES

FILING REQUIREMENTS:

Property in more than one Taxing District - A taxpayer who has property in two or more taxing districts within the same township must file separate returns in each district covering only property located in that district. This is necessary since each taxing district may have different tax rates. [IC

Duplicate Return Requirement - Every taxpayer whose total combined assessed value of business personal property within a single taxing district is $150,000 or more must file each return in duplicate including the confidential returns and schedule attached thererto. See Regulation 16, Rule 2, Sec. 7(a). [IC

Total assessed value of business personal property filed in this taxing district is:

$150,000 or more

Less than $150,000

Multiple Location Taxpayers - Every taxpayer who is required to file in more than one township in the State of Indiana must file a summary form, Form 105 (available from the Department of Local Government Finance or local assessing officials), directly with the Department of Local Government Finance on or before July 15 of the assessment year. (Regulation 16, Rule 2, Sec. 6) [IC

Were expenditures made since March 1 of last year for improvements on any real estate owned, held, possessed, controlled or occupied by the tax- payer in the township wherein this return is filed?  Yes

Yes  No If Yes, attach a statement setting forth: Name of owner, location of real estate and explaining nature, cost, date construction of improvements was begun and date construction was completed. If not completed as of March 1, state the percentage completed at that time. (IC

No If Yes, attach a statement setting forth: Name of owner, location of real estate and explaining nature, cost, date construction of improvements was begun and date construction was completed. If not completed as of March 1, state the percentage completed at that time. (IC

PENALTIES FOR FAILURE TO FILE COMPLETE RETURN FORMS:

Failure to file a return on or before the date, as required by law, will result in the imposition of a

If the total assessed value that a person reports on a personal property return is less than the total assessed value that the person is required by law to report and if the amount of the undervaluation exceeds five percent (5%) of the value that should have been reported on the return, then the county auditor shall add a penalty of twenty percent (20%) of the additional taxes finally determined to be due as a result of the undervaluation.

In completing a personal property return for a year, a taxpayer must make a complete disclosure of all information relating to the value, nature or location of personal property owned, held, possessed or controlled on the assessment date [IC

This information would include, but not be limited to, completion of the heading and related information, answers to all questions and entries on all of the appropriate lines on the face of the return. If such information is not provided, the taxpayer will be contacted and directed to provide that informa- tion. In addition, a penalty of

The above penalties are due on the property tax installment next due for the return whether or not an appeal is filed with the Indiana Tax Court with respect to the tax due on that installment. [IC

Total Tangible Personal Property |

(Please check one) |

|

ASSESSED VALUES |

ASSESSED VALUES BY |

ASSESSED VALUES BY |

|

|

Form 102 |

Form 103 |

|

BY TAXPAYER |

TOWNSHIP ASSESSOR |

PTABOA |

|

|

|

(a) |

|

(b) |

(c) |

Round Assessed Value to Nearest Ten Dollars |

|

$ |

|

$ |

$ |

|

|

|

|

|

|||

|

|

|

|

|

|

|

All vehicles used in farm or business and not subject to Excise Tax must be reported as depreciable personal property in the pools on Schedule A of Forms 102 or 103. All such property used for recreational purposes (not used in business) must be reported on Form 101.

SIGNATURE AND VERIFICATION

Under penalties of perjury, I hereby certify that this return (including accompanying schedules and statements), to the best of my knowledge and belief, is true, correct, and complete; reports all tangible personal property, subject to taxation, owned, held, possessed or controlled by the named taxpayer in the stated township or taxing district on the assessment date of this return, as required by law; and is prepared in accordance with IC

Signature of authorized person |

|

|

|

Please print name |

Date signed (mo., day, yr.) |

|

|

|

|

|

|

||

Title |

Telephone number |

Signature of person preparing return based on all |

Telephone number |

|||

|

( |

) |

information of which he has any knowledge |

|

|

|

|

|

|

( |

) |

||

| Fact | Detail |

|---|---|

| Filing Deadline | This form must be filed with the Township Assessor no later than May 15 unless an extension is granted in writing. |

| Multiplicity Requirement for Taxing Districts | A taxpayer with property in two or more taxing districts within the same township must file separate returns for each district, aligning with IC 6-1.1-3-10(b). |

| Duplicate Return Requirement | Those whose combined assessed value of business personal property in a single district is $150,000 or more must file their return in duplicate, as specified in IC 6-1.1-3-7(c). |

| Requirement for Multiple Location Taxpayers | Taxpayers required to file in more than one township in Indiana must file a summary form (Form 105) with the Department of Local Government Finance by July 15 of the assessment year, according to Regulation 16, Rule 2, Sec. 6 and IC 6-1.1-3-10(a). |

| Penalties | Failure to file or complete return forms can result in a $25 penalty, plus possibly a 20% penalty of the taxes due for late filing beyond 30 days or underreporting assessed value by more than 5%, as per IC 6-1.1-37-7(d) and IC 6-1.1-3-9(a). |

Filling out the Indiana State 104 form, known as the Business Tangible Personal Property Return, is a crucial process for business owners in Indiana. It is a required document for accurately reporting the value of tangible personal property owned, held, possessed, or controlled as of the assessment date. Careful adherence to the submission deadline and thoroughness in completing the form ensures compliance with state laws, potentially sparing business owners from penalties associated with underreporting or late submissions. Following a structured approach can simplify this task considerably.

Following these steps, thoroughly and accurately ensures that the business complies with Indiana's requirements for reporting tangible personal property. It is important to file by the May 15 deadline, or by the end of any extension period granted, to avoid potential penalties. It's equally critical to provide complete and accurate information about the business's property to mitigate the risk of additional penalties for underreportation.

What is the Indiana State Form 104?

The Indiana State Form 104, also known as the Business Tangible Personal Property Return, is a document required to be filed by businesses in Indiana. It details the tangible personal property owned by the business that is subject to taxation. This includes any physical assets used in the business, such as equipment, machinery, and tools.

When is the deadline to file Form 104?

Businesses must submit Form 104 to their Township Assessor by May 15th each year, unless an extension has been granted in writing. This ensures that the assessment and taxation of business personal property are accurately recorded for the fiscal year.

What happens if I file the form late?

Filing Form 104 after the deadline can result in penalties. Initially, a $25.00 penalty is imposed for failing to file on time. If the form is not submitted within 30 days after the due date, an additional penalty equivalent to 20% of the taxes determined to be due on the unreported property will be charged.

Are there any specific requirements for businesses with property in multiple taxing districts?

Yes, if a business owns property in more than one taxing district within the same township, separate returns must be filed for each district. Moreover, businesses whose total assessed value of business personal property in a single taxing district is $150,000 or more are required to file each return in duplicate. Businesses operating in multiple townships across Indiana must also submit a summary form, Form 105, to the Department of Local Government Finance by July 15th.

What information is required on Form 104?

The form requires detailed information about the business and its tangible personal property. This includes the name and address of the business, nature of the business, the location of the property, and a comprehensive list of all taxable personal property. Additionally, any improvements made to real estate since the last assessment date must be reported, including costs and dates of construction.

Can penalties be appealed?

Yes, it is possible to appeal penalties imposed for late filing or underreporting. However, the penalties are due on the next property tax installment, regardless of an ongoing appeal in the Indiana Tax Court regarding the tax due.

How can I avoid penalties for underreported valuations?

To avoid penalties for underreporting the value of tangible personal property, businesses must accurately and completely disclose all relevant information regarding their assets. If the reported value is less than what is legally required by more than 5%, the county auditor will add a penalty of 20% of the additional taxes determined to be due because of the undervaluation.

What are my responsibilities when completing Form 104?

While completing Form 104, businesses are obliged to fully disclose all information relating to their tangible personal property, including value, nature, and location, as of the assessment date. Any improvements made since the preceding assessment date to real property should also be included. Failure to provide complete information may result in penalties and the requirement to submit additional information upon request.

Filling out the Indiana State 104 form, known as the Business Tangible Personal Property Return, is essential for accurately reporting the value of business personal property. Common mistakes can lead to penalties, incorrect assessments, or even legal issues. Recognizing and avoiding these mistakes is crucial for business owners in Indiana.

Not filing by the deadline is a frequent oversight. The form must be submitted to the Township Assessor by May 15, unless an extension has been granted in writing. Missing this deadline results in a penalty of twenty-five dollars ($25.00), and additional penalties may accrue if the delay exceeds thirty days.

Another common error is failing to file separate returns for property in multiple taxing districts within the same township. This is necessary as different districts may have distinctive tax rates, and overlooking this requirement can lead to inaccurate filings and subsequent complications with the Department of Local Government Finance.

Many also overlook the requirement to file returns in duplicate if the total combined assessed value of business personal property within a single taxing district is $150,000 or more. This includes confidential returns and their attached schedules, ensuring that there is a record for both the taxpayer and the assessor's office.

Inaccurate or incomplete disclosures of personal property information can lead to significant penalties. The law requires complete disclosure of all information relating to the value, nature, or location of personal property owned, held, possessed, or controlled on the assessment date. Additionally, any improvements made since the last assessment date must be fully reported. Failure to comply results in penalties and can lead to undervaluation charges.

Some taxpayers make the mistake of not rounding the assessed value to the nearest ten dollars as required by the form's instructions. Though it might seem minor, this precision is necessary for the accuracy of tax assessments and the consistency of records across the board.

Lastly, there is often a failure to sign and date the return, or it's incorrectly done. The signature under penalty of perjury is crucial; it certifies the accuracy of the information provided. Both the signature of the authorized person and the individual preparing the return, if different, are necessary, along with their titles and contact numbers.

Understanding and avoiding these common errors can save Indiana business owners time, prevent financial penalties, and ensure compliance with state tax laws. Vigilance and thoroughness in completing the Indiana State 104 form are essential for a smooth tax reporting process.

Completing business paperwork can often feel like navigating a labyrinth, especially when dealing with tax-related documents. Among these, the Indiana State 104 form, a critical piece for businesses to report their tangible personal property, stands out due to its comprehensive nature and the significance it carries in ensuring compliance with state tax regulations. However, it's rarely the only document a business will handle during the filing process. Several other forms and documents typically accompany or support the filing of the Indiana State 104 form, each serving a unique purpose in the broader context of tax and business reporting.

Understanding the purpose and requirements for each of these documents can significantly streamline the tax filing process for businesses in Indiana. While the Indiana State 104 form serves as the foundational document for reporting business personal property, the additional forms ensure that all aspects of a business’s tangible assets are accurately reflected and assessed. Managing these various elements effectively can help minimize tax liabilities and avoid potential penalties, making it crucial for businesses to stay informed and prepared throughout the filing process.

The Indiana State 104 form, known as the Business Tangible Personal Property Return, is designed for businesses to report their personal property for tax purposes. It captures essential details about a business's tangible assets within a specific township or taxing district. Several other forms share similarities with it, particularly in their purpose, content requirements, and the broader objective of ensuring tax compliance and accurate assessment of business assets.

Form 102 - Tangible Personal Property Assessment Return: Like the Indiana State 104 form, Form 102 is used for reporting tangible personal property owned by a business. Both forms require details such as the nature of the business, location, and the assessed value of the property. Form 102 is specifically designed for initial filings or for businesses not previously assessed, placing an emphasis on capturing a comprehensive snapshot of a business's tangible assets at the onset of its tax obligations.

Form 103 - Short Form for Tangible Personal Property Assessment: This form is a streamlined version intended for businesses with less complex asset reporting needs. While it serves a similar purpose as the Indiana State 104 form, it is simplified, requiring fewer details about the business's personal property. Form 103 is ideal for small businesses or those with straightforward asset portfolios, offering a quicker option for fulfilling their reporting requirements. However, it maintains the core objective of providing a clear account of the business's taxable property.

Form 105 - Summary Form for Multiple Location Taxpayers: Businesses operating across multiple locations or taxing districts within Indiana use Form 105 to summarize their personal property holdings. It complements the Indiana State 104 form by providing an aggregated overview of a taxpayer's assets across various locations. While the 104 form is filed individually for each location, Form 105 collates all these details, ensuring the Department of Local Government Finance can accurately assess the total value of a business's personal property statewide.

These forms work in conjunction to deliver a thorough accounting system for business personal property, ensuring tax compliance and fairness in assessment across Indiana. Each form plays a unique role, yet together, they create a comprehensive framework for business asset declaration and taxation.

Filing the Indiana State Form 104, the Business Tangible Personal Property Return, is a critical process for businesses operating within Indiana. This document plays a vital role in determining the amount of property tax a business will pay. To ensure accuracy and compliance, here are several dos and don'ts a business should consider when completing this form.

Adhering to these guidelines will help ensure that the Business Tangible Personal Property Return for the State of Indiana is filled out accurately and in compliance with state requirements. This not only facilitates a smoother process but also helps mitigate the risk of incurring penalties due to errors or omissions on the form.

Understanding the Indiana State Form 104, also known as the Business Tangible Personal Property Return, is crucial for businesses operating within the state. However, there are several misconceptions surrounding this form that can lead to confusion or even non-compliance. Let's address and clarify some of these common misunderstandings:

Businesses operating in multiple taxing districts need to file separate Form 104 returns for each district. This requirement ensures accurate taxation based on varying district tax rates.

If your business's total combined assessed value of personal property within a single taxing district is $150,000 or more, the law mandates filing each return in duplicate. This includes confidential returns and attached schedules.

For businesses required to file in more than one township in Indiana, summarizing this information on Form 105 and submitting it directly to the Department of Local Government Finance is not optional; it's a strict requirement.

Failure to report any real estate improvements by attaching a detailed statement to your return can result in penalties. Detailed reporting includes the nature, cost, and dates related to the construction of improvements.

The penalties for failing to file or late filing are significant, starting from a $25 penalty to an additional 20% penalty on the taxes due for substantial underreporting or lateness beyond 30 days.

Extensions for filing must be requested and granted in writing. Assuming an extension without official confirmation may lead to the penalties mentioned above.

There's a clear distinction between property used for business, which must be reported on Schedule A of Forms 102 or 103, and recreational property, which must be reported on Form 101. Mixing up these categories can lead to inaccurate reporting.

The form must be signed under penalties of perjury by an authorized person who can certify that all information is complete and true. This ensures accountability and the accuracy of the information provided.

Penalties for incorrect or late filing are applied to the next property tax installment due, regardless of whether an appeal is filed. This means failing to comply promptly can result in financial penalties even as you seek redress.

Correcting these misconceptions is vital for ensuring that your business complies with Indiana's regulations regarding the reporting of tangible personal property. Staying informed and seeking clarification when in doubt can save your business from unnecessary penalties and ensure a smoother reporting process.

When it comes to accurately completing and utilizing the Indiana State 104 form, understanding the requirements and potential penalties is crucial for businesses operating within the state. Below are key takeaways designed to guide taxpayers through this process:

Understanding these critical aspects of the Indiana State 104 form is essential for business owners looking to ensure compliance with state taxation and assessment requirements. Proper attention to deadlines, detailed reporting, and adherence to filing protocols can significantly reduce the risk of penalties and contribute to a smoother assessment process.

Paternity Affidavit Indiana - The process governed by this form is overseen by the Indiana State Department of Health, ensuring it meets state requirements for establishing paternity.

Cf 1 - Sheds light on the significance of the assessor/petitioner conference results in shaping the appeal's direction and the assessment's final determination in Indiana appeals.