Indiana Wh 4 Form in PDF

Indiana Wh 4 Form in PDF

The Indiana WH-4 form, known as the Employee's Withholding Exemption and County Status Certificate, plays a critical role for both employers and employees within the state of Indiana. This document, crucial for accurately determining the amount of state and county income tax withheld from an employee's paycheck, requires detailed personal and financial information. Employees must provide their full name, Social Security Number or ITIN, home address, and the counties of residence and principal employment as of January 1. The form is designed to account for various exemptions that an individual can claim to adjust their withholding. These exemptions include personal and spouse exemptions, dependents, and additional allowances for those 65 or older or blind. Furthermore, the form allows for specification of any additional state or county withholding beyond standard amounts, giving employees control over their tax liabilities throughout the year. The WH-4 form, which must be kept current and updated with the employer for any changes in exemption status or personal circumstances, underscores the shared responsibility between employees and employers in adhering to state tax laws. It’s a vital piece of document ensuring that employees are neither over nor under-withheld for their state and county taxes.

Form

State Form 48845 (R10 /

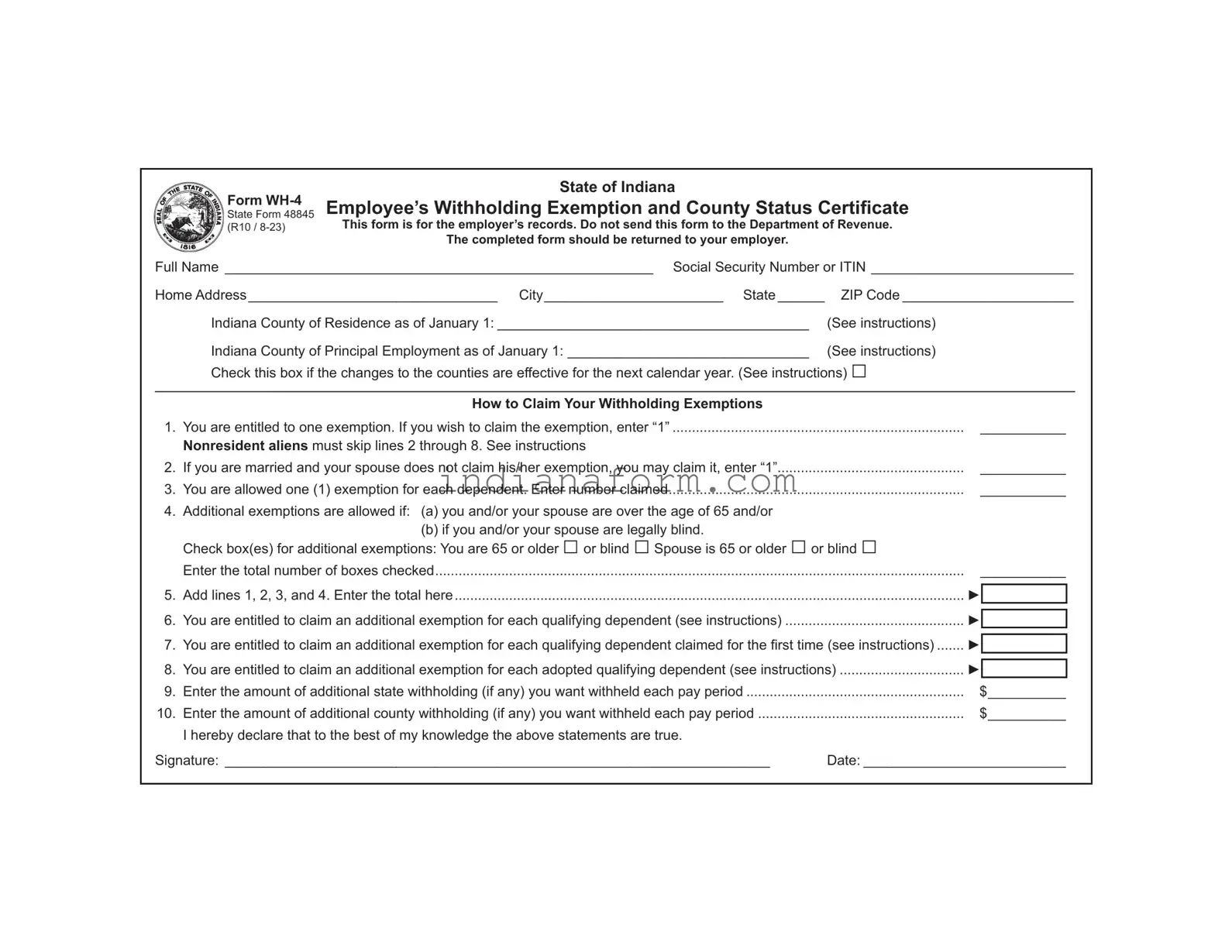

State of Indiana

Employee’s Withholding Exemption and County Status Certificate

This form is for the employer’s records. Do not send this form to the Department of Revenue.

The completed form should be returned to your employer.

Full Name_ _______________________________________________________ Social Security Number or ITIN___________________________

Home Address_________________________________ City_______________________ State_______ |

ZIP Code_______________________ |

||||

|

Indiana County of Residence as of January 1:_________________________________________ |

(See instructions) |

|

|

|

|

Indiana County of Principal Employment as of January 1:________________________________ |

(See instructions) |

|

|

|

|

Check this box if the changes to the counties are effective for the next calendar year. (See instructions) □ |

|

|

|

|

_____________________________________________________________________________________________________________________________________ |

|||||

|

How to Claim Your Withholding Exemptions |

|

|

|

|

1. |

You are entitled to one exemption. If you wish to claim the exemption, enter “1” |

___________ |

|

||

|

Nonresident aliens must skip lines 2 through 8. See instructions |

|

|

|

|

2. |

If you are married and your spouse does not claim his/her exemption, you may claim it, enter “1” |

___________ |

|

||

3. |

You are allowed one (1) exemption for each dependent. Enter number claimed |

___________ |

|

||

4. |

Additional exemptions are allowed if: (a) you and/or your spouse are over the age of 65 and/or |

|

|

|

|

|

(b) if you and/or your spouse are legally blind. |

|

|

|

|

|

Check box(es) for additional exemptions: You are 65 or older □ or blind □ Spouse is 65 or older □ or blind □ |

|

|

|

|

|

Enter the total number of boxes checked |

___________ |

|

||

|

|

|

|

|

|

5. |

Add lines 1, 2, 3, and 4. Enter the total here |

► |

|

|

|

|

|

|

|

||

6. |

You are entitled to claim an additional exemption for each qualifying dependent (see instructions) |

► |

|

|

|

7. |

You are entitled to claim an additional exemption for each qualifying dependent claimed for the first time (see instructions) |

► |

|

|

|

|

|

||||

|

|

|

|||

8. |

.................................You are entitled to claim an additional exemption for each adopted qualifying dependent (see instructions) |

► |

|

|

|

9. |

Enter the amount of additional state withholding (if any) you want withheld each pay period |

$__________ |

|

||

10. |

Enter the amount of additional county withholding (if any) you want withheld each pay period |

$__________ |

|

||

|

I hereby declare that to the best of my knowledge the above statements are true. |

|

|

|

|

Signature:_ ______________________________________________________________________ |

Date:___________________________ |

||||

Instructions for Completing Form

This form should be completed by all resident and nonresident employees having income subject to Indiana state and/or county income tax.

Print or type your full name, Social Security number or ITIN and home address. Enter your Indiana county of residence and county of principal employment as of January 1 of the current year. If you neither lived nor worked in Indiana on January 1 of the current year, enter ‘not applicable’ on the line(s). If you move to (or work in) another county after January 1, your county status will not change until the next calendar year. Please check the box if you are requesting a change to a county of residence or work for the next calendar year.

Nonresident alien limitation. A nonresident alien is allowed to claim only one exemption for withholding tax purposes. If you are a nonresident alien, enter “1” on line 1, then skip to line 9. You are considered to be a nonresident alien if you are not a citizen of the United States and do not meet the green card test and the substantial presence test (get Publication 519 from www.irs.gov for information about these tests).

All other employees should complete lines 1 through 8.

Lines 1 & 2 - You are allowed to claim one exemption for yourself and one for your spouse (if he/she does not claim the exemption for him/herself). If a parent or legal guardian claims you on their federal tax return, you may still claim an exemption for yourself for Indiana purposes. You cannot claim more than the correct number of exemptions; however, you are permitted to claim a lesser number of exemptions if you wish additional withholding to be deducted.

Line 3 - Dependent Exemptions: You are allowed one exemption for each of your dependents based on state guidelines. To qualify as your dependent, a person must receive more than

Line 4 - Additional Exemptions. You are also allowed one exemption each for you and/or your spouse if either is 65 or older and/or blind. Line 5 - Add the total of exemptions claimed on lines 1, 2, 3, and 4. Enter the total in the box provided.

Line 6 - Additional Dependent Exemptions. An additional exemption is allowed for certain dependent children that are included on line 3. The dependent child must be a son, stepson, daughter, stepdaughter, foster child, and/or child for whom you are a legal guardian. The dependent must be under age 19 or must be both under age 24 and a

Line 7 -

Line 8 - Additional Adopted Dependent Exemptions. An additional exemption is allowed for certain dependent children that are included on lines 3 and 6 and have been adopted by you or your spouse. The dependent child must be a son, stepson, daughter, or stepdaughter. The dependent must be under age 19 or must be both under age 24 and a full- time student at a qualified educational institution during at least 5 months of the taxable year.

Lines 9 & 10 - If you would like an additional amount to be withheld from your wages each pay period, enter the amount on the line provided. NOTE: An entry on this line does not obligate your employer to withhold the amount. You are still liable for any additional taxes due at the end of the tax year. If the employer does withhold the additional amount, it should be submitted along with the regular state and county tax withholding.

You may file a new Form

(a)you divorce (or are legally separated from) your spouse for whom you have been claiming an exemption or your spouse claims him/herself on a separate Form

(b)someone else takes over the support of a dependent you claim or you no longer provide more than

(c)a dependent no longer qualifies for an additional dependent or an adopted dependent exemption.

Penalties are imposed for willingly supplying false information or information which would reduce the withholding exemption.

| Fact | Detail |

|---|---|

| Purpose of Form WH-4 | This form is used by employees to declare their withholding exemptions and county status for Indiana state and county income tax purposes. It should be returned to the employer and not sent to the Department of Revenue. |

| Who Needs to Complete It | All resident and nonresident employees who earn income in Indiana that is subject to state and/or county income tax are required to complete this form. |

| Withholding Exemptions | Employees can claim exemptions for themselves, a spouse, dependents, and additional exemptions if they or their spouse are 65 or older and/or legally blind. |

| Updating the Form | Employees must file a new WH-4 form within 10 days if their number of exemptions decreases due to events such as divorce or a dependent no longer qualifying. Attempts to reduce withholding exemptions falsely may result in penalties. |

Completing the Indiana WH-4 form is essential for accurately determining the amount of state and county taxes withheld from your paycheck. This process allows both residents and nonresidents working in Indiana to ensure their employer deducts the correct tax amount based on their personal and dependency status. The steps outlined below guide you through filling out this form, clearly explaining where and what information needs to be provided, ensuring clarity and accuracy in your tax withholdings.

After you have completed the Indiana WH-4 form, remember this document must be submitted to your employer, and not the Department of Revenue. It's your responsibility to update this form if your exemption status changes at any point. This ensures that your state and county tax withholdings remain accurate throughout each tax year.

What is the purpose of the Indiana WH-4 form?

The Indiana WH-4 form is used to determine the amount of state and county income taxes to be withheld from an employee's paycheck. Employees fill out this form so their employer can withhold the correct amount of taxes, reflecting their personal exemption status, and ensuring that both state and county tax obligations are met.

Who needs to complete the Indiana WH-4 form?

All employees in Indiana, whether residents or nonresidents, who receive income that is subject to Indiana state and/or county income tax must complete the form. This includes individuals who live and/or work in Indiana as of January 1 of the current tax year.

Can I claim exemptions for myself and my spouse on the WH-4 form?

Yes, you can claim one exemption for yourself and an additional exemption for your spouse, if they are not claiming their exemption on a separate WH-4 form. This applies even if a parent or legal guardian claims you as a dependent on their federal tax return. You can still claim an exemption for Indiana tax purposes.

How do I claim exemptions for dependents on the Indiana WH-4 form?

You are allowed to claim one exemption for each of your dependents. A qualifying dependent must receive more than half of their financial support from you during the tax year and must not have a gross income exceeding $4,150, unless they are your child under 19 years of age (or under 24 if a full-time student).

What if I or my spouse are 65 or older, or blind?

If you or your spouse are 65 years of age or older, or if either of you is legally blind, you can claim an additional exemption for these conditions on the WH-4 form. Just make sure to check the appropriate boxes and add them to your total exemption count.

Can I change my withholdings later?

Yes, you can file a new WH-4 form at any time if your exemption status changes, such as having more dependents or no longer being able to claim a previously-claimed exemption due to changes in familial or financial circumstances. You are required to submit a new WH-4 within 10 days if your exemptions decrease.

What should nonresident aliens do differently on this form?

Nonresident aliens are limited to claiming only one exemption for withholding tax purposes. They should enter "1" on line 1 and then proceed directly to line 7, skipping the other exemption claims. This is due to specific federal regulations concerning their income tax treatment.

What happens if I supply false information on the WH-4 form?

Supplying false information or intentionally reducing the number of claimed exemptions to reduce tax withholding is subject to penalties. It is important to accurately report your exemption status to avoid potential fines and legal issues.

Do I send the completed WH-4 form to the Indiana Department of Revenue?

No, the completed WH-4 form should be given to your employer for their records. It is not sent to the Indiana Department of Revenue. Your employer will use the information you provide to withhold the appropriate amount of state and county taxes from your paycheck.

What if I have additional amounts I want withheld from my paycheck?

If you wish to have additional taxes withheld beyond the calculated amount based on your exemptions, you can indicate this on lines 7 and 8 for state and county taxes, respectively. However, entering an amount on these lines does not obligate your employer to withhold that additional amount, though it generally will be considered in your withholding.

Filling out the Indiana WH-4 form, which is essential for ensuring the correct amount of state and county taxes are withheld from one's paycheck, can sometimes be tricky. Mistakes on this form may lead to unexpected tax liabilities or over-withheld taxes. When submitting the WH-4, several common errors are made, impacting financial and compliance outcomes.

Avoiding these mistakes requires careful reading of the instructions and understanding one's financial situation. Incorrect or incomplete forms not only impact one's tax situation but also can lead to penalties from the Indiana Department of Revenue. It is advised to review the WH-4 form annually or after any major life events to ensure all the information remains accurate.

Moreover, employees are encouraged to consult with a tax professional if they have questions about how to properly complete the form or if they experience changes in their financial circumstances. An accurate WH-4 form ensures that the right amount of tax is withheld, avoiding surprises during tax season and helping maintain financial stability throughout the year.

When preparing to manage tax responsibilities in Indiana, individuals often encounter the Form WH-4, which is essential for determining the amount of state and county income tax to withhold from an employee's wages. Alongside the WH-4, there are several other important forms and documents that may be required for comprehensive tax filing and employment processes. This information is useful for both employees and employers navigating the complexities of tax documentation.

Understanding and properly managing these forms is crucial for compliance with tax regulations and ensuring employees are correctly documented and taxed according to state and federal laws. Employees benefit from understanding these documents to ensure their withholdings are accurate and to avoid potential issues with tax liabilities. These documents collectively contribute to a systematic and compliant tax filing process for both employers and individuals in Indiana.

The Indiana WH-4 form is similar to the W-4 form used by the federal government for tax withholding purposes. Both forms serve the primary function of informing employers about the amount of tax to withhold from an employee's paycheck. They achieve this through a series of questions that guide employees in declaring their filing status, number of dependents, and any additional amount they wish to have withheld. The key difference lies in their scope of application; the Indiana WH-4 pertains to state and county tax withholdings specific to Indiana, while the W-4 form is used for determining federal income tax withholdings. This design ensures that employees can tailor their withholdings based on both their federal and state tax liabilities, allowing for a more customized approach to tax planning.

Similarly, the Indiana WH-4 form also holds resemblances to the IT-2104 form used by the state of New York for state income tax withholding purposes. Like the Indiana WH-4, New York’s IT-2104 allows employees to indicate their personal allowance and additional withholding preferences, considering their specific state tax obligations. Both forms include sections for personal information, exemption claims for individuals and dependents, and options for additional withholding per pay period. The primary purpose of these forms is to aid employees in avoiding underpayment or overpayment of state taxes through accurate withholding. Despite serving the same fundamental function, each form is tailored to the exemptions, allowances, and tax structures specific to its respective state, highlighting the importance of state-specific forms in the accurate collection and withholding of state income taxes.

When it comes to filling out the Indiana WH-4 form, it's crucial to pay close attention to detail to ensure accurate completion. Let's dive into what you should and shouldn't do to streamline this process effectively.

Things You Should Do:

Things You Shouldn't Do:

By following these dos and don'ts, you’ll be better positioned to fill out your Indiana WH-4 form accurately and efficiently, ensuring your tax withholdings are properly calculated for the year.

The Indiana WH-4 form, an Employee’s Withholding Exemption and County Status Certificate, often evokes a range of misunderstandings among taxpayers. Delving into the nuances of this form helps clarify its purpose and use, ensuring employees accurately fulfill their state tax obligations.

Misconception 1: The form must be filed with the Indiana Department of Revenue. Contrary to this belief, the Indiana WH-4 form should not be sent to the Department of Revenue. Instead, it is intended for the employer's records to determine the correct amount of state and county income tax to withhold from an employee's paycheck.

Misconception 2: Nonresident aliens are excluded from filing the form. While it's true that nonresident aliens have specific instructions, indicating they can claim only one exemption on line 1 and must skip to line 7, they are still required to complete and submit the form to their employer. This ensures that the proper Indiana state and county taxes are withheld.

Misconception 3: You can claim an unlimited number of exemptions. The form limits the number of exemptions an employee can claim. It includes provisions for personal exemptions, dependent exemptions, and exemptions for age or blindness for the taxpayer and spouse. Claiming more exemptions than entitled is incorrect and could lead to penalties.

Misconception 4: The form is only for Indiana residents. While primarily designed for residents, the form must also be completed by nonresidents who have income subject to Indiana state and/or county taxes. This ensures that their taxation is appropriately handled according to Indiana law.

Misconception 5: Once submitted, the WH-4 form cannot be changed. Employees can and should submit a new WH-4 form to their employer whenever their exemption status changes, such as through marriage, divorce, or the birth of a child. This ensures that withholding is always accurate according to the employee's current situation.

Misconception 6: The form affects federal tax withholding. The WH-4 form is specific to Indiana state and county tax withholdings and does not impact the amount of federal tax withheld from an employee’s paycheck. For changes to federal withholdings, a different form, the Federal Form W-4, must be completed.

Misconception 7: Employees decide the additional withholding amount on lines 7 and 8, and employers must comply. While employees can request additional withholding amounts for state and county taxes, it does not obligate the employer to withhold these additional amounts. However, these lines allow employees to adjust their withholdings to better suit their tax situation, potentially avoiding a tax bill at the end of the year.

Understanding the purpose and components of the Indiana WH-4 form is crucial for both employers and employees. It ensures accurate withholding, which can mitigate the risk of unexpected tax liabilities for the employee while keeping employers compliant with Indiana tax laws.

The process of completing and utilizing the Indiana WH-4 form, an essential document for employee tax withholding in the state of Indiana, requires attention to detail to ensure accurate tax withholdings from an employee's paycheck. Several key takeaways should be noted for both employees and employers managing this document.

By carefully completing and, if necessary, periodically updating the Indiana WH-4 form, employees can manage their income tax withholdings more efficiently, ensuring that they neither overpay nor underpay their state and county taxes. Both employers and employees bear responsibility for the accuracy of the information provided on this form, which remains a cornerstone of the tax withholding process in Indiana.

When the Inspection Report Comes In, Which of the Following Should a Buyer's Agent Do? - By delineating a formal response process, the form helps in keeping the property transaction on track, avoiding unnecessary delays and fostering mutual agreement on conditions and terms.

Renew Cna License South Carolina - This form is part of Indiana’s efforts to maintain a high standard of care in long-term care facilities by having a properly certified nursing workforce.

How to Get Your Final Transcript From High School - Reduces the complexities associated with Indiana academic record requests.