Indiana Promissory Note Template

Indiana Promissory Note Template

In the heart of the Midwest, Indiana stands as a beacon of financial dealings and agreements, among which the Promissory Note holds significant importance. This document, crucial for both lenders and borrowers, outlines the promise to pay a specified sum of money by a borrower to a lender. It is tailored to meet the diverse needs of individuals and institutions by laying down the payment terms, interest rates, and what happens if payments are not made as agreed. The form serves as a legally binding agreement, ensuring clarity and understanding between the parties involved and providing a sense of security and trust. Whether it's for personal loans, business ventures, or educational purposes, understanding the nuances of the Indiana Promissory Note form is essential for anyone looking to navigate the complexities of financial transactions within the state. Its role in the financial landscape of Indiana is not only about facilitating loans but also about promoting responsible lending and borrowing practices, thereby contributing to the state’s economic stability.

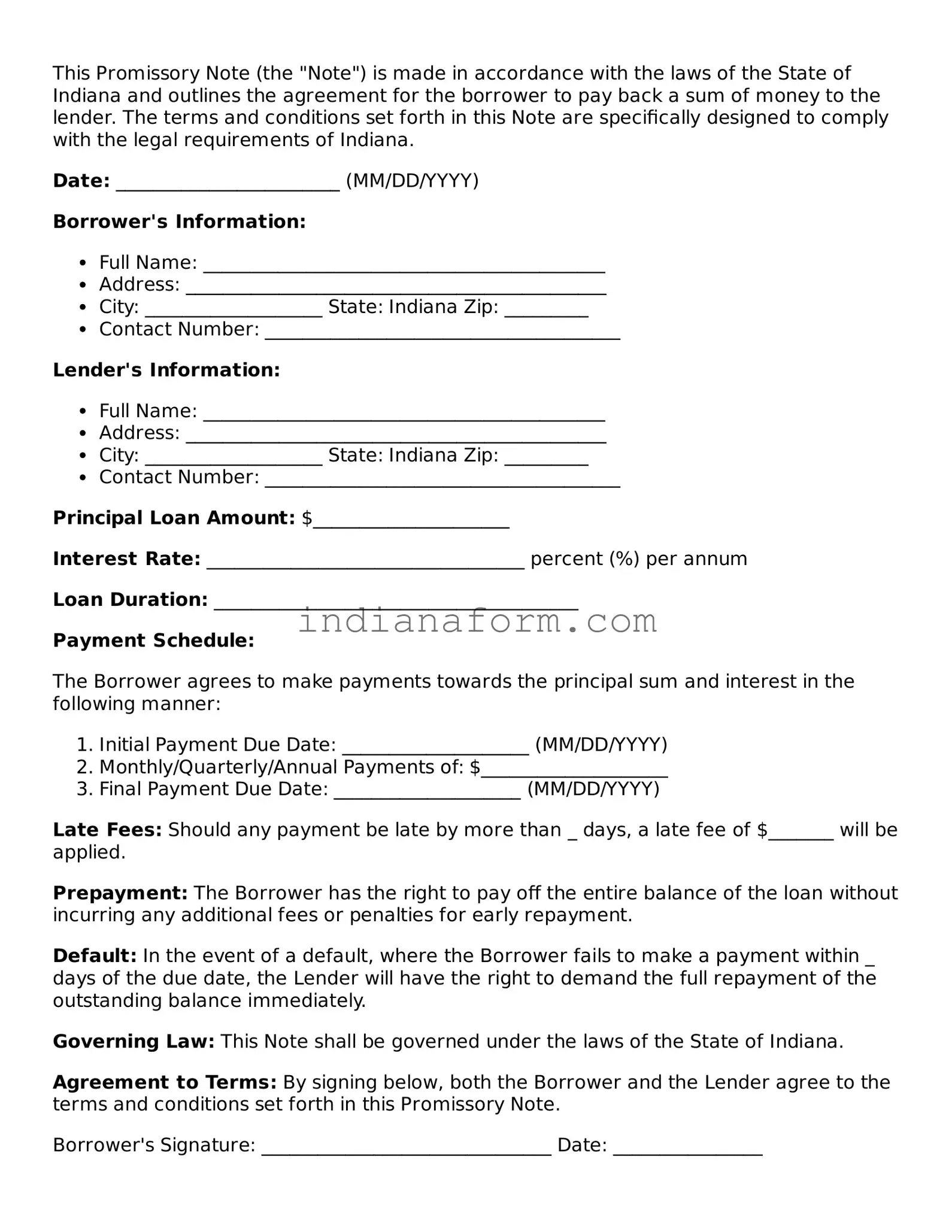

This Promissory Note (the "Note") is made in accordance with the laws of the State of Indiana and outlines the agreement for the borrower to pay back a sum of money to the lender. The terms and conditions set forth in this Note are specifically designed to comply with the legal requirements of Indiana.

Date: ________________________ (MM/DD/YYYY)

Borrower's Information:

Lender's Information:

Principal Loan Amount: $_____________________

Interest Rate: __________________________________ percent (%) per annum

Loan Duration: _______________________________________

Payment Schedule:

The Borrower agrees to make payments towards the principal sum and interest in the following manner:

Late Fees: Should any payment be late by more than _ days, a late fee of $_______ will be applied.

Prepayment: The Borrower has the right to pay off the entire balance of the loan without incurring any additional fees or penalties for early repayment.

Default: In the event of a default, where the Borrower fails to make a payment within _ days of the due date, the Lender will have the right to demand the full repayment of the outstanding balance immediately.

Governing Law: This Note shall be governed under the laws of the State of Indiana.

Agreement to Terms: By signing below, both the Borrower and the Lender agree to the terms and conditions set forth in this Promissory Note.

Borrower's Signature: _______________________________ Date: ________________

Lender's Signature: _________________________________ Date: ________________

This document is a Promissory Note and does not constitute a guarantee of repayment or a legal claim on any specific property as collateral. For the security of both parties, it is recommended to seek legal advice before entering into this agreement.

| Fact | Detail |

|---|---|

| Type of Document | Indiana Promissory Note Form |

| Purpose | To document a loan agreement between a borrower and a lender |

| Governing Law | Indiana Uniform Commercial Code - Article 3 |

| Requirements | Must include the principal loan amount, interest rate, repayment schedule, and signatures of the parties involved |

Completing an Indiana Promissory Note is a formal way to establish the details of a loan agreement between a lender and a borrower in the state of Indiana. This document serves as a legal promise from the borrower to repay the lender under the conditions they agree to, including the loan amount, interest rate, repayment schedule, and any other pertinent terms. Proper completion of this form is critical to ensure its enforceability and to protect the interests of both parties involved. The following steps guide you through filling out the Indiana Promissory Note efficiently and accurately.

Upon successful completion, the Indiana Promissory Note becomes a binding legal agreement. It's important for both parties to keep a copy of the document for their records. This note outlines the commitment of the borrower to repay the lent amount under the agreed terms, making it essential for managing and acknowledging the debt responsibly. Proper creation and maintenance of this document support transparency and trust between the borrower and lender, contributing to a smoother financial transaction and relationship.

What is a Promissory Note in Indiana?

A Promissory Note in Indiana is a legal document that outlines a loan agreement between two parties, typically a lender and a borrower. It specifies the amount of money borrowed, the interest rate, and the repayment plan. This document serves as a formal commitment from the borrower to repay the loan under the terms agreed upon.

Who needs to sign the Indiana Promissory Note?

The Indiana Promissory Note must be signed by the borrower and the lender. In some cases, a co-signer may also be required to sign, especially if the borrower has a limited credit history or income. The signatures formally bind all parties to the terms of the note.

Is a witness or notarization required for an Indiana Promissory Note?

While not always required, having a witness or notarization can add a layer of legal protection and authenticity to the note. It may vary depending on the amount loaned and the preference of the parties involved. For larger loans or more formal agreements, notarization is recommended to ensure the note's enforceability.

What happens if the borrower does not repay the loan as agreed in the Promissory Note in Indiana?

If the borrower fails to repay the loan according to the terms set in the Promissory Note, the lender has the right to pursue legal action to recover the owed amount. This may include filing a lawsuit to seek repayment or initiating foreclosure proceedings if the loan is secured by collateral.

Can you modify an Indiana Promissory Note after it’s been signed?

Yes, an Indiana Promissory Note can be modified after it's been signed, but any changes must be agreed upon by all parties involved. The modifications should be made in writing, and the document should be signed again by the borrower, the lender, and any co-signers to ensure that the new terms are enforceable.

Are there different types of Promissory Notes in Indiana?

Yes, there are mainly two types of Promissory Notes in Indiana: secured and unsecured. A secured promissory note is backed by collateral, such as real estate or a vehicle, which the lender can claim if the borrower defaults on the loan. An unsecured promissory note does not involve collateral, which poses a higher risk to the lender.

How is the interest rate determined for a Promissory Note in Indiana?

The interest rate on a Promissory Note in Indiana is agreed upon by the borrower and the lender at the time of the loan's origination. It must comply with Indiana's usury laws, which cap the maximum interest rate that can be charged on loans to prevent unlawful or excessive interest rates.

Does a Promissory Note need to be filed or registered with any government body in Indiana?

No, a Promissory Note in Indiana does not need to be filed or registered with a government body. However, maintaining copies of the signed and dated document is crucial for both parties for record-keeping and in case of any future disputes.

What should you do if you lose your original Indiana Promissory Note?

If the original Indiana Promissory Note is lost, it’s important to contact all parties involved immediately. You may draft a new note to be signed as a replacement, or create a written and signed statement detailing the loss and affirming the terms of the original note to maintain the agreement's validity.

When filling out an Indiana Promissory Note form, mistakes can be easy to make but costly to correct. A promissory note is a crucial financial document, laying out the terms under which one party promises to repay a debt to another. Being mindful of common pitfalls can streamline the process and ensure the agreement is legally binding and clear to all parties involved.

The first mistake often involves inaccurate information. Accuracy is paramount when detailing the names of parties, the amount borrowed, and repayment terms. An incorrect name or amount can invalidate the entire agreement or lead to significant misunderstandings.

Another common error is failing to specify the interest rate. In Indiana, if an interest rate is not mentioned, the state's default interest rate applies. However, this rate may not be favorable to the lender, making it important to clearly state the agreed-upon interest rate.

Omitting repayment terms is also a significant oversight. The agreement should include how often payments are to be made (monthly, quarterly, etc.), the amount of each payment, and when the first payment is due. Without this information, the note might not be enforceable.

Many individuals also neglect to include late payment fees or consequences of non-payment. These details protect the lender by incentivizing timely payments and detailing recourse if the borrower fails to pay as agreed.

Forgetting to stipulate the governing state laws can lead to confusion, especially if the parties reside in different states. Since laws vary by state, including a clause about which state's law governs the note clarifies how disputes will be resolved.

Some people make the mistake of not having the note witnessed or notarized. While this isn’t always a legal requirement, it adds a layer of authenticity and can help enforce the document if disputes arise.

Lastly, failure to keep a signed copy of the note is surprisingly common. Both the lender and borrower should have their own signed copies for their records. Without this, enforcing the agreement or proving its existence becomes challenging.

Ensuring that these common mistakes are avoided when filling out the Indiana Promissory Note form can save time, money, and stress for both the borrower and the lender. By paying close attention to the details and legal requirements, the parties involved can create a strong, enforceable agreement that reflects their intentions and protects their interests.

The Indiana Promissory Note form is a crucial document for formalizing the agreement between a borrower and a lender regarding the loan terms. When dealing with financial transactions and agreements, it's often necessary to have additional documents ready to ensure all aspects of the transaction are well-documented and legally binding. Below is a list of documents that are commonly used in conjunction with the Indiana Promissory Note form to fortify the agreement, provide additional legal protections, and clarify the expectations of all parties involved.

Together, these documents provide a comprehensive framework that supports the initial Promissory Note, making the entire process transparent and legally enforceable. Each document serves its purpose in protecting the interests of all parties involved and helps prevent potential disputes by clearly setting out the terms and conditions of the financial agreement. It's important for both lenders and borrowers to understand the significance of these additional documents and use them appropriately to ensure the smooth execution of their financial transactions.

The Indiana Promissory Note form is similar to other legal documents that create a binding agreement between parties. These documents are essential in various contexts, including personal loans, business deals, and real estate transactions. This form, specifically, is akin to a loan agreement, a mortgage note, and an IOU, each serving a distinctive yet related purpose in the sphere of agreements that govern the terms of repayment for borrowed funds.

Loan Agreement

The Indiana Promissory Note and a Loan Agreement share common ground as they both are utilized to outline the terms under which money is lent. The similarities lie in their detailed description of the loan's conditions, including the interest rate, repayment schedule, and the consequences of a default. However, a Loan Agreement typically encompasses a broader scope of clauses, such as warranties, covenants, and borrower certifications, making it more comprehensive. The Indiana Promissory Note, by contrast, tends to be simpler and more straightforward, focusing primarily on the repayment terms.

Mortgage Note

Comparable to the Indiana Promissory Note, a Mortgage Note is a promise to repay a specified sum of money plus interest at a defined rate. The key similarity between these two documents is their function as a pledge to pay under the terms agreed upon by the borrower and the lender. A Mortgage Note, however, is specifically secured by a mortgage loan, which means it's tied to a piece of real estate as collateral. This distinction highlights how a Mortgage Note not only details the repayment obligations but also embeds the legal framework that allows the lender to foreclose on the property if the borrower fails to meet the terms of the agreement.

IOU

An IOU is another document that shares characteristics with the Indiana Promissory Note, albeit more informal. Both serve as written acknowledgments of debt, but an IOU is usually less detailed and lacks specific terms of repayment. It typically states who owes money to whom, but might not include information on interest rates, repayment dates, or the consequences of non-repayment. Despite these differences, both documents are legally binding under certain conditions and signify the borrower's commitment to repay the lender, establishing a mutual understanding of the debt owed.

When filling out the Indiana Promissory Note form, it is crucial to approach the task with attention and care. A promissory note is a binding legal document that commits the borrower to repay a specified sum of money to the lender under agreed-upon terms. Below, find a list of do's and don'ts to help guide you through this process efficiently and effectively:

By adhering to these guidelines, parties can execute a promissory note with confidence, knowing that they have taken the necessary steps to protect their interests and comply with Indiana law.

When it comes to the Indiana Promissory Note form, several misconceptions can lead to confusion. Understanding these misunderstandings is crucial to correctly using and interpreting these forms. Here's a clear breakdown:

Only used for large loans: Many people believe that promissory notes are only for significant loan amounts. In reality, they can be used for loans of any size, providing a legally binding agreement for repayment terms between two parties, no matter the amount.

Legally binding without signatures: A common misconception is that a promissory note is legally binding once it is written and agreed upon. However, without the borrower's and lender's signatures, the document does not usually hold legal weight in Indiana courts.

Does not require witness or notarization: While not all promissory notes require a witness or notarization to be considered valid, having them can add a layer of protection and credibility to the agreement, especially in the event of a dispute.

Interest rates are unregulated: Another misunderstanding is that the interest rates on a promissory note can be set freely. Indiana, like many states, has usury laws that limit the maximum interest rate a lender can charge, thereby protecting borrowers from excessively high rates.

Informal agreements are just as effective: Some believe that a verbal agreement or an informal written agreement can serve the same purpose as a promissory note. However, without the formal structure and specific elements of a promissory note, these informal agreements may not provide the same level of legal protection or clarity.

No need for specific details: Lastly, there is a misconception that a promissory note does not need to include specific details about the loan. In fact, including detailed information about the loan amount, interest rate, repayment schedule, and any collateral ensures clear understanding and expectations from both parties, reducing the potential for conflict.

When dealing with the Indiana Promissory Note form, it's important to grasp its significance and ensure accuracy in its completion. Here are five key takeaways to bear in mind:

In essence, when completing the Indiana Promissory Note form, attention to detail and a clear understanding of the legal requirements are paramount. Proper preparation and execution lay the groundwork for a legally binding agreement that safeguards the interests of all parties involved.

Indiana Dnr Form - It's a legal document that assures your end-of-life care preferences are respected by healthcare providers.

Quit Claim Deed Form Indiana - Ensuring the accuracy of a deed form is critical, as errors can complicate or invalidate property transfers.