State 38337 Form in PDF

State 38337 Form in PDF

In the realm of financial obligations that insurance companies operating within Indiana must navigate, the State Form 38337 stands as a crucial document. Crafted to guide the quarterly submission of estimated premiums and the associated tax, this form demands meticulous attention to detail and strict adherence to deadlines, as outlined by the Indiana Department of Insurance. Companies are tasked with not only calculating these estimates based on prior year figures but also adjusting for current year activities, thereby ensuring both compliance and fiscal responsibility. With the form's stringent requirement for typewritten submissions and the rounding of all values to the nearest dollar, accuracy is paramount. Adding to the complexity, each company must submit separate checks and forms for every entity under its banner, exclusively to the designated Bank Lockbox, highlighting the state's emphasis on organized and efficient processing. Moreover, the form accommodates specific dates by which submissions must be received—April 15, June 15, September 15, and December 15—while also offering provisions for submissions when due dates fall on weekends or holidays. The allowed methods of dispatch include only select postal services, reinforcing the importance of timely and secure delivery. Completing this form accurately serves as a testament to an insurer's commitment to regulatory compliance, showcasing an understanding of their fiscal duties towards the state's regulatory framework for insurance operations.

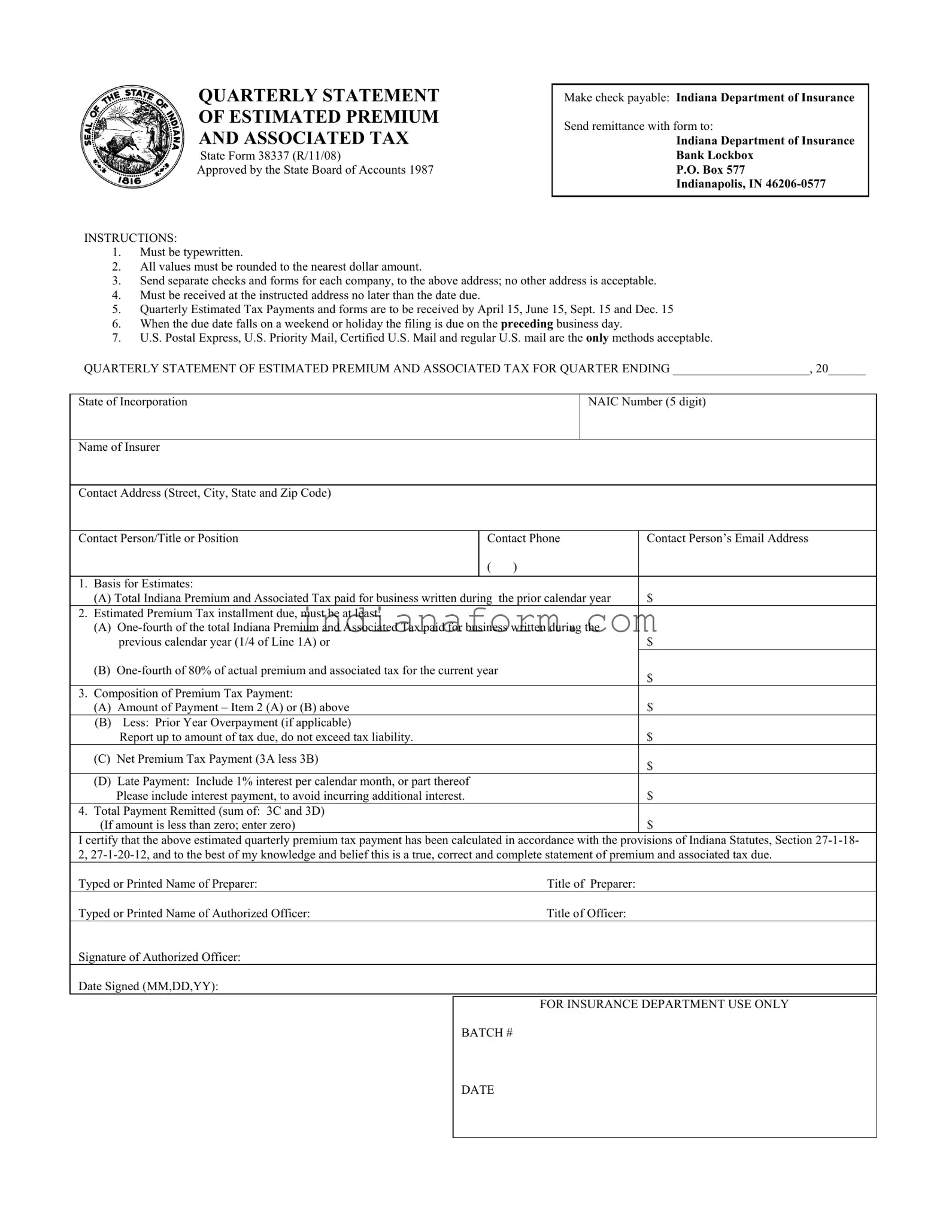

QUARTERLY STATEMENT OF ESTIMATED PREMIUM AND ASSOCIATED TAX

State Form 38337 (R/11/08)

Approved by the State Board of Accounts 1987

Make check payable: Indiana Department of Insurance

Send remittance with form to:

Indiana Department of Insurance

Bank Lockbox

P.O. Box 577

Indianapolis, IN

INSTRUCTIONS:

1.Must be typewritten.

2.All values must be rounded to the nearest dollar amount.

3.Send separate checks and forms for each company, to the above address; no other address is acceptable.

4.Must be received at the instructed address no later than the date due.

5.Quarterly Estimated Tax Payments and forms are to be received by April 15, June 15, Sept. 15 and Dec. 15

6.When the due date falls on a weekend or holiday the filing is due on the preceding business day.

7.U.S. Postal Express, U.S. Priority Mail, Certified U.S. Mail and regular U.S. mail are the only methods acceptable.

QUARTERLY STATEMENT OF ESTIMATED PREMIUM AND ASSOCIATED TAX FOR QUARTER ENDING ______________________, 20______

State of Incorporation |

|

|

NAIC Number (5 digit) |

||

|

|

|

|

|

|

Name of Insurer |

|

|

|

|

|

|

|

|

|

|

|

Contact Address (Street, City, State and Zip Code) |

|

|

|

|

|

|

|

|

|||

Contact Person/Title or Position |

Contact Phone |

Contact Person’s Email Address |

|||

|

|

( |

) |

|

|

|

|

|

|

|

|

1. Basis for Estimates: |

|

|

|

|

|

(A) Total Indiana Premium and Associated Tax paid for business written during |

the prior calendar year |

$ |

|||

2. Estimated Premium Tax installment due, must be at least: |

|

|

|

|

|

(A) |

|

||||

|

previous calendar year (1/4 of Line 1A) or |

|

|

|

$ |

(B) |

|

|

$ |

||

|

|

|

|

|

|

3. Composition of Premium Tax Payment: |

|

|

|

|

|

(A) Amount of Payment – Item 2 (A) or (B) above |

|

|

|

$ |

|

(B) Less: Prior Year Overpayment (if applicable) |

|

|

|

|

|

|

Report up to amount of tax due, do not exceed tax liability. |

|

|

|

$ |

(C) Net Premium Tax Payment (3A less 3B) |

|

|

|

$ |

|

|

|

|

|

|

|

(D) |

Late Payment: Include 1% interest per calendar month, or part thereof |

|

|

|

|

|

Please include interest payment, to avoid incurring additional interest. |

|

|

|

$ |

4. Total Payment Remitted (sum of: 3C and 3D) |

|

|

|

|

|

(If amount is less than zero; enter zero) |

|

|

|

$ |

|

I certify that the above estimated quarterly premium tax payment has been calculated in accordance with the provisions of Indiana Statutes, Section

Typed or Printed Name of Preparer: |

Title of Preparer: |

Typed or Printed Name of Authorized Officer: |

Title of Officer: |

Signature of Authorized Officer: |

|

Date Signed (MM,DD,YY): |

|

|

|

|

FOR INSURANCE DEPARTMENT USE ONLY |

|

BATCH # |

DATE

| Fact | Detail |

|---|---|

| Form Type | State Form 38337: Quarterly Statement of Estimated Premium and Associated Tax |

| Issuing Authority | Indiana Department of Insurance |

| Submission Deadlines | Quarterly Estimated Tax Payments and forms are due on April 15, June 15, September 15, and December 15. If a due date falls on a weekend or holiday, filings are due on the preceding business day. |

| Penalty for Late Payment | Includes 1% interest per calendar month, or part thereof, on late payments. |

| Governing Laws | Indiana Statutes, Section 27-1-18-2, 27-1-20-12 govern the preparation and submission of this form. |

Filing the State 38337 form, a Quarterly Statement of Estimated Premium and Associated Tax, is a required process for insurance companies operating within specific regulatory frameworks. It ensures timely and accurate payment of estimated premium taxes to the Indiana Department of Insurance, keeping companies compliant with state mandates. Carefully following the outlined steps will streamline the submission process, aiding in the avoidance of common mistakes such as incorrect rounding of figures, late submissions, and the misdirection of remittance, thus preventing unnecessary penalties or interest charges.

Upon completion, the insurance company has taken a necessary step in fulfilling state regulatory responsibilities. Timely and accurate completion and submission of the State 38337 form help ensure that companies remain in good standing, avoiding potential fines or operational hiccups. Constant attention to detail and adherence to the specified deadlines will contribute to a smoother regulatory compliance process.

What is the State 38337 form used for?

The State 38337 form is used by insurance companies to submit their quarterly statement of estimated premium and associated tax to the Indiana Department of Insurance. This form helps in calculating and remitting the due taxes for insurance premiums collected within Indiana.

How should the State 38337 form be prepared?

This form must be typed and rounded to the nearest dollar amount to ensure accuracy. It's important to follow the instructions carefully to avoid errors in submission.

Where and to whom do I make the check payable when submitting the State 38337 form?

Make the check payable to the Indiana Department of Insurance. Ensure that your remittance, alongside the completed form, is sent to the specified Bank Lockbox address in Indianapolis, as indicated on the form.

Are there specific deadlines for submitting the State 38337 form?

Yes, the quarterly estimated tax payments and forms must be received by April 15, June 15, September 15, and December 15. If the due date falls on a weekend or holiday, the submission is due on the preceding business day.

What if I have multiple companies? Can I send one check and form for all?

No, you must send separate checks and forms for each company. This ensures that each company's payment is accurately processed and recorded.

What methods of mail are acceptable for sending the State 38337 form?

The only accepted methods of mail are U.S. Postal Express, U.S. Priority Mail, Certified U.S. Mail, and regular U.S. mail. Using these methods ensures your submission is received securely and on time.

How is the estimated premium tax installment calculated?

Your estimated premium tax installment can be calculated in two ways: either as one-fourth of the total Indiana premium and associated tax paid for business written during the previous calendar year or as one-fourth of 80% of the actual premium and associated tax for the current year. Choose the method that applies to your situation.

What should I do if I have made an overpayment in the previous year?

If there's been an overpayment, you can deduct this amount from your current payment due. However, the report up to the amount of tax due should not exceed your tax liability.

What happens if my payment is late?

In case of a late payment, include 1% interest per calendar month, or part of a month, on the overdue amount to avoid incurring additional interest. This helps to cover the state's administrative costs for late submissions.

Who needs to sign the State 38337 form?

The form must be signed by an authorized officer of the insurance company. The signature, along with the officer's title, certifies that the information provided is accurate and calculated in accordance with Indiana Statutes.

Filling out government forms can feel like navigating through a maze, and the State Form 38337 for the Quarterly Statement of Estimated Premium and Associated Tax is no exception. This form, while critical for insurance companies operating in Indiana, often trips up even the most meticulous of preparers. Here are ten common mistakes to avoid when completing this form.

Not typing the form. The very first instruction specifies that the form must be typewritten. Handwritten submissions can lead to processing delays or even rejections.

Rounding errors are another common pitfall. All values must be rounded to the nearest dollar amount. Failing to do so can result in incorrect tax calculations.

Sending a combined payment for multiple companies. Each company's check and form must be sent separately to ensure proper attribution and processing.

Using an incorrect address. The form strictly instructs that remittances are to be sent only to the designated lockbox address. Other addresses will not process these forms.

Missing the due date. Payments and forms are due on specific quarterly dates. Late submissions can attract penalties.

Overlooking the adjusted due date rule. When due dates fall on weekends or holidays, submissions are due the preceding business day. This is a frequently missed detail.

Choosing an unauthorized mailing method. Only specific types of mail are accepted, and using another method could prevent your form from being received on time.

Incorrect tax calculations. This mistake can occur if the preparer does not correctly apply one-fourth of the total Indiana Premium and Associated Tax paid during the previous year, or one-fourth of 80% of the current year's actual premiums and associated tax.

Failure to account for prior year overpayments properly. If applicable, such overpayments can reduce the amount of current tax due, but they should not exceed the current tax liability.

Excluding late payment interest. If a payment is made after its due date, including the correct interest calculation is essential to avoid accruing additional interest.

Avoiding these mistakes involves a careful reading of the form's instructions, precise calculations, and attention to detail. Here are some tips for steering clear of errors:

By familiarizing yourself with these common slip-ups and adhering to the form's instructions, the process of completing and submitting the State Form 38337 should become smoother and more efficient, helping your company stay compliant with Indiana's regulatory requirements.

When preparing and submitting the State Form 38337 for Quarterly Statement of Estimated Premium and Associated Tax, various other forms and documentation are often required to ensure compliance and accuracy in reporting. These supplemental documents play a critical role in the insurance financial reporting process, helping to provide a comprehensive view of an insurance company's obligations and financial condition. Understanding each document's purpose can significantly streamline the reporting process and ensure adherence to regulatory requirements.

Together, these documents form a network of financial and regulatory reporting that supports and enhances the information provided through the State Form 38337. Familiarity with each document ensures that insurance providers can accurately assess and report their tax liabilities, thereby maintaining compliance with state regulations and contributing to the overall financial stability of the insurance industry. Proper documentation and timely submissions uphold the integrity of financial reporting and assist in avoiding potential penalties or audits by regulatory authorities.

The State 38337 form, with its focus on the quarterly statement of estimated premium and associated tax, shares similarities with a few key documents utilized in various financial reporting contexts. Each of these documents serves a unique purpose but parallels can be drawn in their structure, usage, and the type of information they require.

Federal Form 941, Employer's Quarterly Federal Tax Return: Much like the State 38337 form, Federal Form 941 is used to report quarterly taxes, specifically federal withholdings from employees for income, social security, and Medicare taxes. Both forms necessitate detailed financial calculations based on recent activities, require submission by specific quarterly deadlines, and impose penalties for late submissions. Form 941, however, is focused on payroll taxes collected by employers, whereas the State 38337 form pertains to the insurance industry's estimated premium taxes.

State Sales Tax Filing Forms: These forms vary by state but generally require businesses to report and remit taxes collected on sales within the state for a given period, often quarterly. Similar to the State 38337 form, sales tax forms are periodic (usually quarterly), require calculation of taxes owed based on specific rates, and include penalties for late payment. While State 38337 focuses on insurance premiums, sales tax forms cover a broader range of transactions, demonstrating their versatility across different types of businesses.

Form 1040-ES, Estimated Tax for Individuals: This form allows individuals to calculate and pay their estimated taxes on a quarterly basis. Like the State 38337 form, Form 1040-ES is used for estimating and paying taxes in advance to avoid penalties. Both necessitate an understanding of tax obligations and encourage timely payments. However, 1040-ES is designed for individual taxpayers, covering income such as wages, dividends, and self-employment earnings, contrasting the corporate focus of the State 38337 form.

When preparing the State 38337 form, "Quarterly Statement of Estimated Premium and Associated Tax," it's crucial to follow specific dos and don'ts to ensure the process is completed accurately and efficiently. Here is a curated list of ten recommendations to aid in this process:

Do:Ensure all information is typewritten to maintain clarity and prevent misinterpretation.

Round all values to the nearest dollar amount for consistency and accuracy.

Send separate checks and forms for each company to keep records distinct and manageable.

Use only U.S. Postal Express, U.S. Priority Mail, Certified U.S. Mail or regular U.S. mail for delivery to guarantee the acceptance of your documents.

Adhere strictly to the due dates (April 15, June 15, Sept. 15, and Dec. 15) to avoid penalties or interest for late submissions.

Avoid sending payments to any address other than the specified Indiana Department of Insurance Bank Lockbox to ensure your payment is processed correctly.

Do not underestimate the convenience of typewritten entries over handwritten ones, as legibility can significantly affect processing times and accuracy.

Refrain from rounding off figures to more or less than the nearest dollar, since precise values are necessary for accurate financial reporting.

Avoid delaying until the last moment to submit your form and payment; plan for possible delays to meet the submission deadlines.

Do not forget to include any applicable interest for late payments to avoid further interest accrual or penalties.

Following these recommendations can simplify the submission process and help ensure compliance with the State's requirements. Moreover, managing this process with accuracy and punctuality could help avoid unnecessary delays or financial discrepancies.

When dealing with the State Form 38337, which pertains to the Quarterly Statement of Estimated Premium and Associated Tax, there are several misconceptions that may lead to confusion or errors. Understanding these misconceptions can help ensure compliance and accuracy when preparing and submitting this important document.

Addressing these misconceptions head-on can significantly smooth out the process of complying with the requirements set forth by the Indiana Department of Insurance. Careful attention to the form's instructions not only aids in correct submission but also helps avoid unnecessary delays or financial penalties.

Filling out and using the State Form 38337, known as the Quarterly Statement of Estimated Premium and Associated Tax, is an important procedure for insurance companies operating in Indiana. This document is crucial for reporting and paying premium taxes on a quarterly basis. Here are some key takeaways to help ensure that the process is completed accurately and on time.

In addition to these key points, it's also essential to accurately calculate the estimated premium tax payment based on previous years' data or the current year's projected figures, subtract any overpayment from the prior year, and include interest for late payments. This comprehensive approach helps to ensure that the quarterly tax obligations are met both accurately and punctively. Lastly, ensure that the form is signed by an authorized officer and that the submission includes the correct payment amounts. By following these guidelines, companies can navigate the process of reporting and paying premium taxes in Indiana with confidence.

Written Permission Printable Hunting Permission Form - By setting clear expectations and legal boundaries, the form contributes to a safer hunting environment.

Ccdf Meaning - This form allows parents and guardians in Indiana to apply for the Child Care and Development Fund (CCDF), which subsidizes the cost of child care from accredited providers.