State 49585 Form in PDF

State 49585 Form in PDF

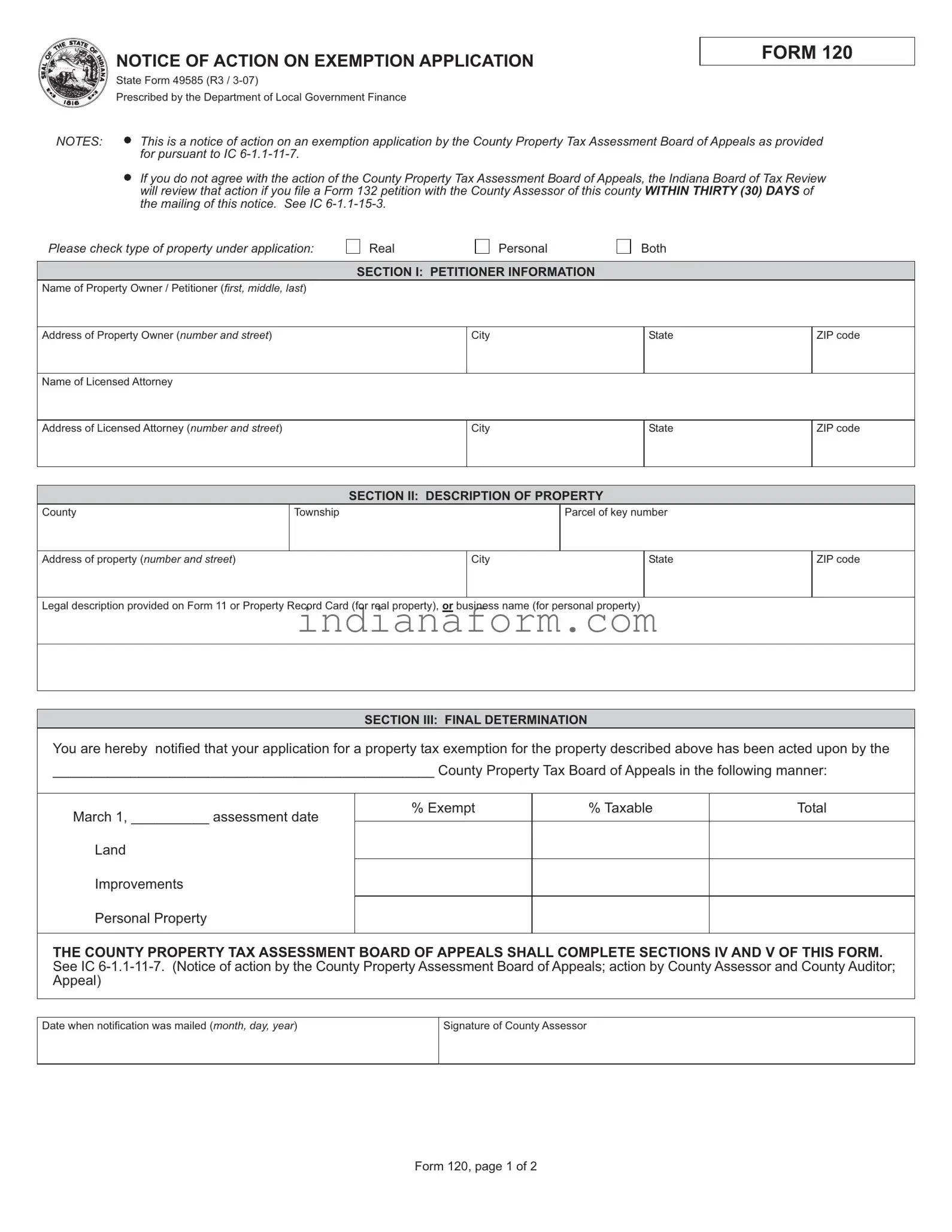

The State 49585 form, titled "NOTICE OF ACTION ON EXEMPTION APPLICATION," serves as a crucial communication tool between the County Property Tax Assessment Board of Appeals and property owners seeking a tax exemption. This document, outlined by the Department of Local Government Finance and following the guidelines pursuant to IC 6-1.1-11-7, notifies property owners about the action taken on their exemption applications. It highlights the importance of timely responses, specifying that any disagreements with the board's decision must be challenged through the filing of a Form 132 petition with the County Assessor within 30 days of notice receipt. The form comprehensively requires details regarding the petitioner's information, including the property owner's name and address, as well as the contact details of their licensed attorney if applicable. It also asks for a description of the property under consideration, whether real, personal, or both, alongside the final determination of the exemption application by the County Property Tax Assessment Board of Appeals. This determination includes the assessment date, percentage of tax exemption granted, and the breakdown of value between land improvements and personal property. Additionally, reasons for the board's decision and requisite signatures are mandated for completeness. This form not only facilitates a transparent assessment and appeals process but also ensures property owners are well-informed of their rights and the steps needed to contest decisions if necessary.

NOTICE OF ACTION ON EXEMPTION APPLICATION

State Form 49585 (R3 /

Prescribed by the Department of Local Government Finance

FORM 120

NOTES: |

This is a notice of action on an exemption application by the County Property Tax Assessment Board of Appeals as provided |

|

for pursuant to IC |

If you do not agree with the action of the County Property Tax Assessment Board of Appeals, the Indiana Board of Tax Review will review that action if you file a Form 132 petition with the County Assessor of this county WITHIN THIRTY (30) DAYS of the mailing of this notice. See IC

Please check type of property under application:

Real

Personal

Both

SECTION I: PETITIONER INFORMATION

Name of Property Owner / Petitioner (first, middle, last)

Address of Property Owner (number and street) |

City |

State |

ZIP code |

|

|

|

|

Name of Licensed Attorney |

|

|

|

|

|

|

|

Address of Licensed Attorney (number and street) |

City |

State |

ZIP code |

|

|

|

|

SECTION II: DESCRIPTION OF PROPERTY

County |

Township |

|

Parcel of key number |

|

|

|

|

|

|

|

|

Address of property (number and street) |

|

City |

|

State |

ZIP code |

|

|

|

|

|

|

Legal description provided on Form 11 or Property Record Card (for real property), or business name (for personal property) |

|

||||

SECTION III: FINAL DETERMINATION

You are hereby notified that your application for a property tax exemption for the property described above has been acted upon by the

_________________________________________________ County Property Tax Board of Appeals in the following manner:

March 1, __________ assessment date |

% Exempt |

% Taxable |

Total |

|

|

|

|

|

|

|

|

Land |

|

|

|

Improvements |

|

|

|

Personal Property |

|

|

|

|

|

|

|

|

|

|

|

THE COUNTY PROPERTY TAX ASSESSMENT BOARD OF APPEALS SHALL COMPLETE SECTIONS IV AND V OF THIS FORM. See IC

Date when notification was mailed (month, day, year) |

Signature of County Assessor |

|

|

Form 120, page 1 of 2

SECTION IV: DETERMINATION BY COUNTY PROPERTY TAX ASSESSMENT BOARD OF APPEALS

The County Property Tax Assessment Board of Appeals’ determination is based on the following reasons. This statement should include cites to applicable statutes, regulations, or case law in support of this determination.

SECTION V: SIGNATURES

Signature of County Property Tax Assessment Board of Appeals member

Date signed (month, day, year)

Signature of County Property Tax Assessment Board of Appeals secretary

Date signed (month, day, year)

Form 120, page 2 of 2

| Fact | Detail |

|---|---|

| Form Name | State Form 49585 (R3 / 3-07) |

| Prescribed by | Department of Local Government Finance |

| Purpose | Notice of action on an exemption application by the County Property Tax Assessment Board of Appeals |

| Governing Law | IC 6-1.1-11-7 |

| Appeal Process | File a Form 132 petition with the County Assessor within thirty (30) days of the mailing of the notice for review by the Indiana Board of Tax Review |

| Type of Property | Allows for specification of Real, Personal, or Both types of property |

| Sections | Includes Petitioner Information, Property Description, Final Determination, and Determination by County Property Tax Assessment Board of Appeals |

| Final Determination | Details the percentage of property exempt and taxable as determined by the County Property Tax Assessment Board of Appeals |

| Required Signatures | Requires signatures from both the County Property Tax Assessment Board of Appeals member and secretary |

| Supporting Documents | Must include legal description provided on Form 11 or Property Record Card for real property, or business name for personal property |

Filling out the State 49585 form is a crucial step in the process of seeking a decision on an exemption application. This document ensures that individuals seeking exemptions are informed about the actions taken by the County Property Tax Assessment Board of Appeals. Completing this form accurately is essential for the next steps in the process, especially if the petitioner disagrees with the decision. In that case, a Form 132 petition must be filed with the County Assessor within 30 days of receiving this notice. By following these steps, individuals can ensure their case is processed efficiently and correctly.

Once the form is fully filled out and submitted, it's essential to keep a close eye on the calendar. If there's a need to file an appeal, remember that the Form 132 petition must be submitted within 30 days of the mailing date of this notice. Ensuring all details are accurate and submitted timely can significantly impact the review process of your application.

What is the State Form 49585?

State Form 49585, also known as the Notice of Action on Exemption Application, is a document issued by the County Property Tax Assessment Board of Appeals. This form serves as a notification regarding the board's decision on an application for property tax exemption in Indiana. It is used for both real and personal property tax exemption applications.

Who should receive the State Form 49585?

The form is mailed to property owners or petitioners who have applied for a property tax exemption. If a petitioner has a licensed attorney, a copy may also be sent to the attorney's address. It provides the applicants with the board's decision on their exemption request.

What actions can I take if I disagree with the decision?

If you disagree with the decision of the County Property Tax Assessment Board of Appeals, you have the right to appeal. An appeal can be filed by submitting a Form 132 petition to the County Assessor within 30 days from the mailing date of the notice.

What information is included in the State Form 49585?

The form includes the petitioner's information, a description of the property in question, and the final determination of the exemption application. The determination section will indicate the percentage of the property that is exempt and taxable, along with the decision on land improvements and personal property if applicable.

How is the determination made by the Board detailed in the form?

The determination made by the County Property Tax Assessment Board of Appeals is detailed in the form, including reasons for the decision. This section may cite applicable statutes, regulations, or case law that support the determination.

What sections of the State Form 49585 must be completed by the County Property Tax Assessment Board of Appeals?

Sections IV and V of the form must be completed by the County Property Tax Assessment Board of Appeals. These sections include the determination and reason for the decision, along with the signatures and dates signed by the board's member and secretary.

What does it mean if my property is categorized as % Exempt and % Taxable?

The categories of % Exempt and % Taxable in the final determination indicate the portions of your property that are exempt from property taxes and those that are subject to taxation. If your property is partially exempt, this will reflect how much of your property's value is taxable and how much is exempt from property taxes.

Is there a deadline for filing an appeal if I disagree with the exemption decision?

Yes, there is a strict deadline for filing an appeal. You must file a Form 132 petition with the County Assessor of your county within 30 days of the mailing of the State Form 49585. It is important to act quickly if you wish to appeal the decision.

Filling out Form 49585, the Notice of Action on Exemption Application, is a critical step for property owners looking to secure tax exemptions in the state. However, even small errors can significantly delay or affect the outcome of an application. Here are ten common mistakes to avoid:

Avoiding these common errors requires attention to detail and a full understanding of the form's requirements. Applicants are encouraged to thoroughly review their application before submission to ensure the best chance of approval. Remember, accuracy and completeness are key.

Understanding and navigating through the process of filing tax exemption applications can be challenging. Applicants must stay diligent, double-check each part of the form, and adhere to deadlines and submission guidelines. With careful preparation and attention to detail, the likelihood of a successful tax exemption application increases significantly.

When dealing with property tax exemptions and the appeals process in Indiana, the State 49585 Form, known as the Notice of Action on Exemption Application, is a crucial document. However, this process typically requires navigating through additional paperwork to ensure that a property owner’s or petitioner’s case is thoroughly presented or to comply with legal requirements. Here’s a look at other forms and documents often used in tandem with the State 49585 Form for a comprehensive approach to handling property tax matters.

Navigating the property tax exemption and appeal process requires a thorough understanding and timely management of various forms and supporting documents. Each piece of documentation plays a specific role in building a comprehensive case for exemption or appealing an unsatisfactory decision by the tax authorities. Careful attention to detail and adherence to deadlines are critical for property owners seeking favorable outcomes in their property tax dealings.

The State 49585 form, titled NOTICE OF ACTION ON EXEMPTION APPLICATION, shares similarities with other documents used within the realm of property taxation and legal appeals. While each form serves a specific purpose within the tax appeal process or property evaluation, their functions and the information they require provide a basis for comparison.

One such document is the Form 11: Property Tax Assessment Notice. Like the State Form 49585, Form 11 is issued by local property tax assessors to inform property owners of the assessed value of their property, which is crucial for determining tax liabilities. Both forms play a pivotal role in the property tax assessment and appeals process, providing property owners with essential information on valuation or exemption status. However, while Form 49585 notifies owners of the decision on an exemption application, Form 11 details the assessed value of a property that can be contested through an appeal.

Another document that bears resemblance is the Form 132: Petition for Review of Assessment. This form is directly linked to the State Form 49585, as mentioned within its content. Property owners who disagree with the decision documented in the State Form 49585 regarding their exemption application can file Form 132 to initiate a review by the Indiana Board of Tax Review. Both forms are integral components of the appeal process, with Form 49585 serving as the triggering document for any disputes over exemption decisions, and Form 132 acting as the means through which such disputes are formally raised and reviewed.

In addition, the Property Record Card shares a vital connection with the information provided in State Form 49585. While not a formal appeal or notification form like the others, the Property Record Card contains detailed information on the property's characteristics and valuation basis, which could be relevant to an exemption application's outcome. The State Form 49585 indirectly references this document through its requirement for a legal description of the property, which can be found on the Property Record Card. Together, these documents contribute to a comprehensive understanding of a property's valuation and tax status, facilitating informed decisions and appeals by property owners.

When dealing with the process of filling out the State Form 49585, an application concerning property tax exemptions, it's crucial to navigate the procedure with precision and awareness. Here are key dos and don'ts that might help guide you through this task with ease and accuracy.

Do's:

Don'ts:

Many people find the process of applying for a property tax exemption confusing, and misconceptions about State Form 49585 - the Notice of Action on Exemption Application - are common. Let's clear up some of these misunderstandings.

It's just a formality and doesn't require action. This is a misconception. When you receive State Form 49585, it means a decision has been made regarding your exemption application. If you disagree with this decision, you have 30 days to file a Form 132 petition for review. Ignoring this notice can mean missing the opportunity to appeal.

Anyone can fill out and submit the form. While it's true that any property owner can submit an application, it’s important to note that the form itself is not submitted by the individual. Instead, it is a notice sent by the County Property Tax Assessment Board of Appeals to inform you of the action taken on your application.

The form covers all types of exemptions. State Form 49585 specifically relates to property tax exemptions. It’s not a catch-all for every kind of tax exemption or appeal. The exemptions in question pertain to real or personal property.

Legal representation is not necessary for the process. While you're not required to have a licensed attorney, having one can be beneficial, especially if you decide to appeal the board's decision. The form even includes a section for attorney information, emphasizing the importance of professional guidance.

There’s plenty of time to appeal the decision. Actually, the window for filing an appeal is quite narrow. You have only 30 days from the mailing of the notice. This limited timeframe emphasizes the importance of promptly reviewing the decision and consulting with professionals if needed.

The form is the final step in the exemption process. Receiving the form is not the end. If you decide to appeal, it’s only part of an ongoing process that includes filing a Form 132 petition and potentially presenting your case to the Indiana Board of Tax Review.

Filing an appeal is a complex and tedious process. While the process of appealing might seem daunting, it is structured to ensure that property owners have a fair chance to contest decisions. Carefully following instructions and possibly getting legal advice can make this process manageable.

The decision is based purely on the board's discretion. This isn't accurate. The Board of Appeals' final determination is grounded in the law, as they must base their decisions on applicable statutes, regulations, or case law, and provide reasons for their determination on the form.

Understanding State Form 49585 and the associated procedures is crucial for property owners seeking exemptions. By dispelling these misconceptions, property owners can better navigate the process and take appropriate action when necessary.

Understanding the State 49585 form is crucial for any individual or entity seeking an exemption on property taxes in Indiana. The form, serving as a notice of action on an exemption application, outlines the decision made by the County Property Tax Assessment Board of Appeals on such applications. Below are key takeaways to help navigate the process effectively:

Navigating the completion and implications of the State 49585 form requires attention to detail and an understanding of the legal framework governing property tax exemptions in Indiana. By closely following the guidelines and meeting the prescribed deadlines, petitioners can ensure their rights are adequately represented and protected throughout the process.

State 44905 - State Form 44905 provides a systematic approach to managing paper clutter and ensuring efficient use of space in government offices.

Indiana Tax Forms 2023 - Direct deposit options are available for receiving refunds, with spaces for routing and account numbers.

When the Inspection Report Comes In, Which of the Following Should a Buyer's Agent Do? - It specifies how the seller should reply to the buyer's requests or concerns raised through the inspection, including agreeing to repairs or rejecting the demands.