State Of Indiana 130 Short Form in PDF

State Of Indiana 130 Short Form in PDF

The State of Indiana 130 Short Form is an essential document for property owners seeking to appeal their property tax assessments. This form, formally known as the "Petition for Review of Assessment by Local Assessing Official - Property Tax Assessment Board of Appeals," serves as a vital avenue for taxpayers to dispute their property assessments. It encompasses a wide range of information and steps necessary for the filing and processing of an appeal. Property owners are required to specify the type and details of the property under dispute, whether it is real or personal property, alongside the assessment year they are appealing. The form outlines the circumstances under which a taxpayer can seek a review, including deadlines for filing an appeal and detailed instructions on the appeal process. This process involves meetings with county or township officials, hearings before the Property Tax Assessment Board of Appeals, and the potential to further appeal to the Indiana Board. Taxpayers are instructed on the necessary documentation and information that must accompany their appeal, including their primary contentions regarding the assessment. The instructions emphasize the importance of timely filing, the rights of the taxpayer throughout the appeal process, and the potential outcomes of an appeal. Additionally, the form cautions that the appeal could result in an increased, decreased, or unchanged assessment, underscoring the seriousness and implications of the appeal process.

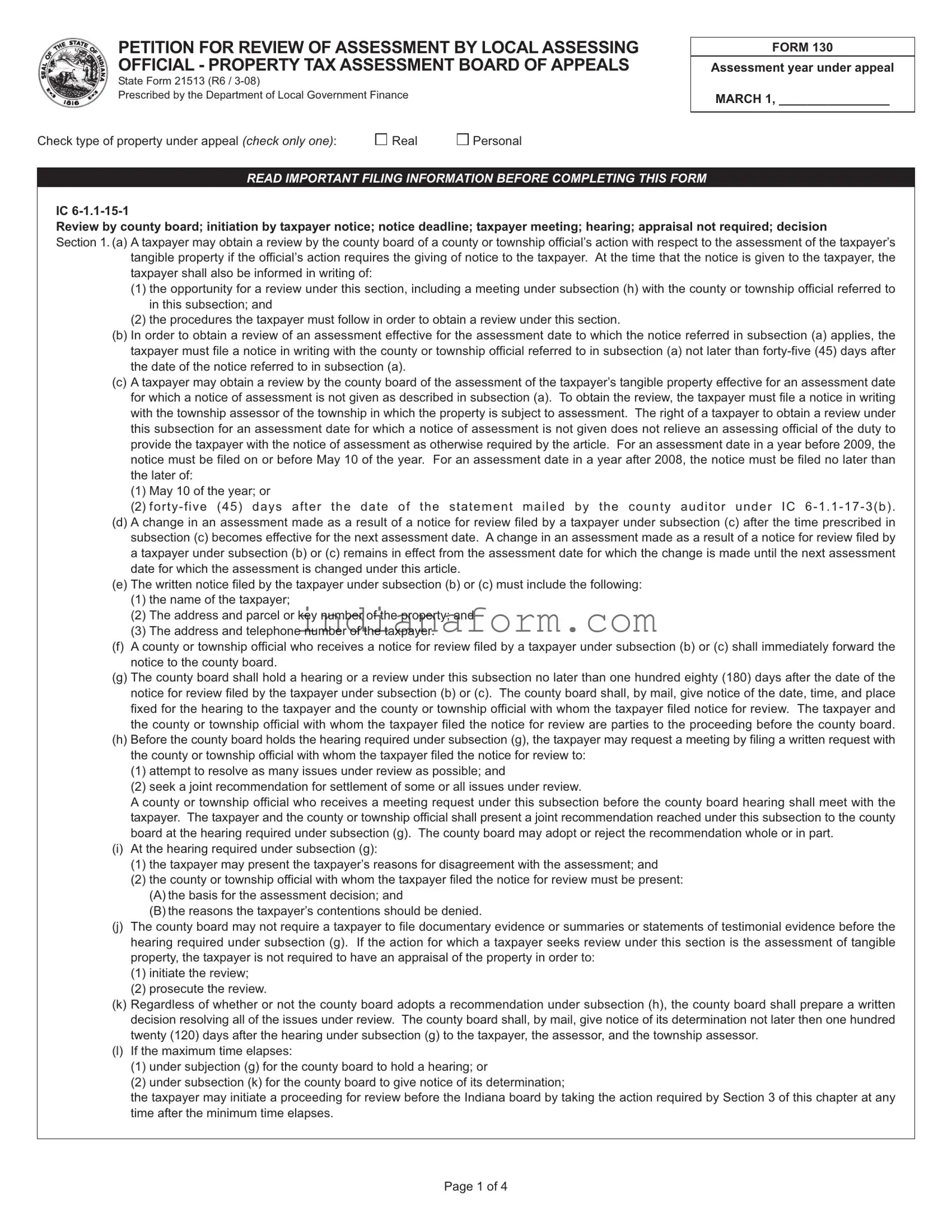

PETITION FOR REVIEW OF ASSESSMENT BY LOCAL ASSESSING OFFICIAL - PROPERTY TAX ASSESSMENT BOARD OF APPEALS

State Form 21513 (R6 /

Prescribed by the Department of Local Government Finance

Check type of property under appeal (check only one): |

Real |

Personal |

FORM 130

Assessment year under appeal

MARCH 1, ________________

READ IMPORTANT FILING INFORMATION BEFORE COMPLETING THIS FORM

IC

Review by county board; initiation by taxpayer notice; notice deadline; taxpayer meeting; hearing; appraisal not required; decision

Section 1. (a) A taxpayer may obtain a review by the county board of a county or township official’s action with respect to the assessment of the taxpayer’s tangible property if the official’s action requires the giving of notice to the taxpayer. At the time that the notice is given to the taxpayer, the taxpayer shall also be informed in writing of:

(1)the opportunity for a review under this section, including a meeting under subsection (h) with the county or township official referred to in this subsection; and

(2)the procedures the taxpayer must follow in order to obtain a review under this section.

(b)In order to obtain a review of an assessment effective for the assessment date to which the notice referred in subsection (a) applies, the taxpayer must file a notice in writing with the county or township official referred to in subsection (a) not later than

(c)A taxpayer may obtain a review by the county board of the assessment of the taxpayer’s tangible property effective for an assessment date for which a notice of assessment is not given as described in subsection (a). To obtain the review, the taxpayer must file a notice in writing with the township assessor of the township in which the property is subject to assessment. The right of a taxpayer to obtain a review under this subsection for an assessment date for which a notice of assessment is not given does not relieve an assessing official of the duty to provide the taxpayer with the notice of assessment as otherwise required by the article. For an assessment date in a year before 2009, the notice must be filed on or before May 10 of the year. For an assessment date in a year after 2008, the notice must be filed no later than the later of:

(1)May 10 of the year; or

(2) forty - five (45) days after the date of the statement mailed by the county auditor under IC 6 - 1 . 1 - 17 - 3(b) .

(d)A change in an assessment made as a result of a notice for review filed by a taxpayer under subsection (c) after the time prescribed in subsection (c) becomes effective for the next assessment date. A change in an assessment made as a result of a notice for review filed by a taxpayer under subsection (b) or (c) remains in effect from the assessment date for which the change is made until the next assessment date for which the assessment is changed under this article.

(e)The written notice filed by the taxpayer under subsection (b) or (c) must include the following:

(1)the name of the taxpayer;

(2)The address and parcel or key number of the property; and

(3)The address and telephone number of the taxpayer.

(f)A county or township official who receives a notice for review filed by a taxpayer under subsection (b) or (c) shall immediately forward the notice to the county board.

(g)The county board shall hold a hearing or a review under this subsection no later than one hundred eighty (180) days after the date of the notice for review filed by the taxpayer under subsection (b) or (c). The county board shall, by mail, give notice of the date, time, and place fixed for the hearing to the taxpayer and the county or township official with whom the taxpayer filed notice for review. The taxpayer and the county or township official with whom the taxpayer filed the notice for review are parties to the proceeding before the county board.

(h)Before the county board holds the hearing required under subsection (g), the taxpayer may request a meeting by filing a written request with the county or township official with whom the taxpayer filed the notice for review to:

(1)attempt to resolve as many issues under review as possible; and

(2)seek a joint recommendation for settlement of some or all issues under review.

A county or township official who receives a meeting request under this subsection before the county board hearing shall meet with the taxpayer. The taxpayer and the county or township official shall present a joint recommendation reached under this subsection to the county board at the hearing required under subsection (g). The county board may adopt or reject the recommendation whole or in part.

(i)At the hearing required under subsection (g):

(1)the taxpayer may present the taxpayer’s reasons for disagreement with the assessment; and

(2)the county or township official with whom the taxpayer filed the notice for review must be present:

(A)the basis for the assessment decision; and

(B)the reasons the taxpayer’s contentions should be denied.

(j)The county board may not require a taxpayer to file documentary evidence or summaries or statements of testimonial evidence before the hearing required under subsection (g). If the action for which a taxpayer seeks review under this section is the assessment of tangible property, the taxpayer is not required to have an appraisal of the property in order to:

(1)initiate the review;

(2)prosecute the review.

(k)Regardless of whether or not the county board adopts a recommendation under subsection (h), the county board shall prepare a written decision resolving all of the issues under review. The county board shall, by mail, give notice of its determination not later then one hundred twenty (120) days after the hearing under subsection (g) to the taxpayer, the assessor, and the township assessor.

(l)If the maximum time elapses:

(1)under subjection (g) for the county board to hold a hearing; or

(2)under subsection (k) for the county board to give notice of its determination;

the taxpayer may initiate a proceeding for review before the Indiana board by taking the action required by Section 3 of this chapter at any time after the minimum time elapses.

Page 1 of 4

IMPORTANT FILING INFORMATION (continued)

IC

Review by Indiana board; initiation by petition of taxpayer or county assessor; petition deadline and form; appraisal not required; decision

Section 3.(a) A taxpayer may obtain a review by the Indiana board of a county board's action with respect to the following:

(1)The assessment of that taxpayer's tangible property if the county board's action requires the giving of notice to the taxpayer.

(2)The exemption of that taxpayer's tangible property if the taxpayer receives a notice of an exemption determination by the county board under IC

(b)The county assessor is the party to the review under this section to defend the determination of the county board. At the time the notice of that determination is given to the taxpayer, the taxpayer shall also be informed in writing of:

(1)the taxpayer's opportunity for review under this section; and

(2)the procedures the taxpayer must follow in order to obtain review under this section.

(c)A county assessor who dissents from the determination of an assessment or an exemption by the county board may obtain a review of the assessment or the exemption by the Indiana board.

(d)In order to obtain a review by the Indiana board under this section, the party must, not later than

(1)file a petition for review with the Indiana board; and

(2)mail a copy of the petition to the other party.

(e)The Indiana board shall prescribe the form of the petition for review of an assessment determination or an exemption by the county board. The Indiana board shall issue instructions for completion of the form. The form and the instructions must be clear, simple, and understandable to the average individual. A petition for review of such a determination must be made on the form prescribed by the Indiana board. The form must require the petitioner to specify the reasons why the petitioner believes that the assessment determination or the exemption determination by the county board is erroneous.

(f)If the action for which a taxpayer seeks review under this section is the assessment of tangible property, the taxpayer is not required to have an appraisal of the property in order to do the following:

(1)Initiate the review.

(2)Prosecute the review.

GENERAL INSTRUCTIONS:

1.Please print or type.

2.The petitioner should complete Section I, Section II, and Section III of this form.

3.The petition must be signed by the petitioner or an authorized representative. A representative must attach a notarized power of attorney unless the representative is a duly authorized employee of corporate officer of the taxpayer.

Is a power of attorney attached? |

Yes |

No |

4.Certified tax representatives must attach a Tax Representative Disclosure statement. 50 IAC

As a result of filing this petition, the assessment may increase, may decrease, or may stay the same.

SECTION I: PROPERTY & PETITIONER INFORMATION

County |

Township |

Parcel or key number (for real property only) |

|

|

|

|

|

Address of property being appealed (number and street, city state, and ZIP code) |

|

|

|

|

|

|

|

Legal description on Form 11 or Property Record card (for real property), or business name (for personal property) |

|

|

|

|

|

|

|

Name of property owner |

|

Telephone number of property owner |

|

|

|

( |

) |

|

|

|

|

Mailing address of property owner (number and street, city state, and ZIP code) |

|

|

|

|

|

|

|

Name of authorized representative (if different from owner) |

|

Telephone number of authorized representative |

|

|

|

( |

) |

|

|

|

|

Mailing address of authorized representative (number and street, city state, and ZIP code)

Page 2 of 4

SECTION II: REASON FOR APPEAL

Land |

Improvements |

Personal Property |

The property described in Section I is currently assessed at:

The petitioner contends that the property should be assessed at:

Present use for the property

Use for which property was designed

Classification of property (commercial, residential, etc.)

Was property sold in the last three years? |

|

If yes, date of sale (month, day, year) |

Sale price |

Yes |

No |

|

|

|

|

|

|

If the property was sold in the last three years, attach the purchase agreement, escrow statement, closing statement, or other evidence, if available. If buyer and seller were or are related or had any common business interests, attach an explanation of the relationship.

If the property was not sold but was listed for sale in the past three years, attach a copy of the listing agreement or other available evidence.

Do you intend to present the testimony or report of a professional assessor / appraiser?

Yes |

No |

Is the property valued higher than comparable properties?

Yes

No

If yes, attach the owner’s name and address of each comparable property and explain how the property is comparable to the property being appealed.

The requested change in assessed value is justified for the following reasons: (Give specific reasons. Do not give conclusions such as the assessment is too high.)

SECTION III: SIGNATURES

Petitioner, taxpayer, or duly authorized employee or corporate officer of the taxpayer

I certify that my entries in Section I and Section II are accurate to the best of my knowledge and belief. I also understand that by appealing my assessment, my assessment may increase, may decrease, or may remain the same.

Signature of petitioner, taxpayer, or duly authorized officer

Date of signature (month, day, year)

Printed or typed name of petitioner, taxpayer, or duly authorized officer

Tax representative

I certify that the entries in Section I and Section II are accurate to the best of my knowledge and belief. I certify that I have viewed this property, the property record card, and Form 11 or Form 113, and that I have the authority to file this appeal on behalf of the taxpayer. I certify that I have made all necessary disclosures to my client, pursuant to 50 IAC

Signature of tax representative

Date of signature (month, day, year)

Printed or typed name of tax representative

Attorney representative

I certify that my entries in Section I and Section II are accurate to the best of my knowledge and belief.

Signature of attorney representative

Date of signature (month, day, year)

Printed or typed name of attorney representative

CHECKLIST

I have reviewed Form 11 RA, Form 11 CI, or Form 113. I have reviewed the property record card.

If I am appealing both real and personal property assessments, I have filed separate petitions for each property. I have checked the type of property under appeal (real or personal) at the top of page one.

I have completed Section I, Section II, and Section III of this petition.

I have given specific reasons for the requested change in value in Section II of this petition.

If this petition is being filed by an authorized tax representative, a duly executed power of attorney and a Tax Representative Disclosure statement is attached. I have signed this petition.

I understand that I must submit the original and one copy of this form to the assessing official. If there are other related parcels currently under appeal, a listing of these parcels is attached.

Page 3 of 4

FOR ASSESSING OFFICIAL USE ONLY

1. Date notice was sent to taxpayer (month, day, year) |

2. Date petition for review was filed by petitioner (month, day, year) |

3. Petition for review timely filed? |

|

|

|

Yes |

No |

|

|

|

|

Signature of assessor |

Date of signature (month, day, year) |

|

|

|

|

|

|

If the answer to number 3 above is “No”, the assessor shall notify the petitioner that the petition was not timely filed.

THE FOLLOWING SECTION IS FOR THE ASSESSOR / PETITIONER CONFERENCE

SECTION IV: RESULTS OF ASSESSOR / PETITIONER CONFERENCE

Before the county board holds the hearing required under IC

(1)attempt to resolve as many issues under review as possible; and

(2)seek a joint recommendation for settlement of some or all of the issues under review.

A county or township official who receives a meeting request under this subsection before the county board hearing shall meet with the taxpayer. The taxpayer and the county or township official shall present a joint recommendation reached under this subsection to the county board at the hearing required under IC

Land |

Improvements |

Personal Property |

The petitioner contends that the property should be assessed at:

The assessing official contends that the property should be assessed at:

If no agreement can be reached, explain the reasons for disagreement. If a change in assessed value is being made, explain the reason for the change.

SIGNATURES

The values listed above and the explanation given accurately reflect my opinion regarding this property.

Signature of assessing official

Date of signature (month, day, year)

Printed or typed name of assessing official

Signature of taxpayer or authorized representative

Date of conference (month, day, year)

Printed or typed name of taxpayer or authorized representative

Page 4 of 4

| Fact | Detail |

|---|---|

| Form Name | Petition for Review of Assessment by Local Assessing Official - Property Tax Assessment Board of Appeals |

| State Form Number | 21513 (R6 / 3-08) |

| Prescribed by | Department of Local Government Finance |

| Applicable Law | IC 6-1.1-15-1, IC 6-1.1-15-3 |

| Type of Property Under Appeal | Real or Personal (Check only one) |

| Assessment Year Under Appeal | MARCH 1, ________ (Year to be filled by petitioner) |

| Important Filing Dates | Notice for review must be filed within 45 days post notice for assessments after the referred date or by May 10 of the year for assessments before 2009. For years after 2008, no later than the latter of May 10 or 45 days after statement mailing by county auditor under IC 6-1.1-17-3(b). |

| Documentary Evidence | No requirement to file documentary evidence before the hearing; appraisal not required for initiating or prosecuting the review. |

| Review Process | Ensures a written decision by the county board within 120 days post-hearing, with provisions for review by the Indiana Board if timelines are not met. |

| General Instructions | Requires detailed property and petitioner information, reason for appeal, and must be signed by the petitioner or an authorized representative. |

If you're looking to challenge your property tax assessment in Indiana, completing the State Form 130 Short Form, officially known as the "Petition for Review of Assessment by Local Assessing Official - Property Tax Assessment Board of Appeals," is your first step. This document allows property owners to present their case to the local Board of Appeals, potentially leading to a change in their property's assessed value. The process involves providing detailed information about the property, stating reasons for the appeal, and possibly engaging in a review meeting or hearing. Here's how to fill out the form properly:

After submitting the form, your case will be reviewed by the county or township official, and a hearing or review meeting will be scheduled. This is your opportunity to present your case and potentially influence the assessed value of your property. Always ensure that your contact information is accurate and that you promptly respond to any correspondence or requests for additional information from the assessing office or the Property Tax Assessment Board of Appeals.

What is the State of Indiana 130 Short Form?

The State of Indiana 130 Short Form, also known as the "Petition for Review of Assessment by Local Assessing Official - Property Tax Assessment Board of Appeals," is a document prescribed by the Indiana Department of Local Government Finance. Its main purpose is to facilitate the process whereby a taxpayer can appeal the assessment of their tangible property, whether it's real or personal property, as made by a local assessing official. It outlines the procedure for appealing to the Property Tax Assessment Board of Appeals.

Who should file the State Form 130?

Any taxpayer who disagrees with the assessment of their tangible property by a county or township official should file the State Form 130. This applies to both real property (such as land and buildings) and personal property (such as business equipment).

When is the deadline to file State Form 130?

The deadline to file a State Form 130 varies depending on whether a notice of assessment has been given. If a notice was issued, the taxpayer must file a written notice with the county or township official no later than forty-five (45) days after the date of the notice. For an assessment date for which no notice was provided, the deadline for filing is generally May 10 of the year following the assessment or forty-five (45) days after the county auditor mails a statement, depending on which is later.

What happens after filing the form?

Upon receipt of the State Form 130, the county or township official will forward the form to the county board, which will then schedule a hearing or review no later than one hundred eighty (180) days after receiving the taxpayer's notice for review. The county board will send a notification including the date, time, and place of the hearing to both the taxpayer and the assessing official.

Can I request a meeting before the hearing?

Yes, before the official hearing, the taxpayer has the opportunity to request a meeting with the county or township official by filing a written request. This meeting aims to resolve issues, seek settlements, and potentially avoid a formal hearing process. Any joint recommendation reached during this meeting will be presented at the hearing.

Is an appraisal required to file or proceed with the appeal?

No, the taxpayer is not required to have an appraisal of the property to initiate or prosecute the appeal. This is aligned with the intent to make the process as accessible as possible to taxpayers without necessitating additional financial expenditures.

What should be included in the written notice filed by the taxpayer?

The written notice should include the taxpayer's name, the address and parcel or key number of the property, and the address and telephone number of the taxpayer. This information is essential for processing the appeal.

What if the deadline for a decision passes?

If the county board does not hold a hearing within 180 days or does not provide a determination within 120 days post-hearing, the taxpayer has the right to initiate a proceeding for review before the Indiana Board. This can be done anytime after the minimum time required for the county board's action elapses.

Can the assessment change as a result of filing this petition?

Yes, as a result of filing the petition, the assessment of the property may either increase, decrease, or remain the same. It's important for taxpayers to understand this possibility when deciding to appeal an assessment.

Filling out the State of Indiana 130 Short Form, a crucial document for appealing property tax assessments, can be tricky. Here are common pitfalls people might encounter:

These mistakes can be avoided by thoroughly reading the instructions, checking and double-checking all entered information, and ensuring that all required documentation is attached before submission. A clear understanding of the appeal process and the form's requirements can significantly improve your chances of a successful appeal.

In addition to avoiding these common errors, remember the general instructions section, which emphasizes the need to print or type clearly, complete all required sections, and attach a notarized power of attorney if filing through a representative. Attention to these details can further streamline the process, minimizing delays or the risk of rejection.

Being meticulous and prepared when filling out the State of Indiana 130 Short Form can lead to a smoother appeal process and potentially favorable outcomes in adjusting your property tax assessment.

When navigating the complexities of property tax appeals in Indiana, utilizing the State Form 21513 (R6 / 3-08), also known as the State Of Indiana 130 Short Form, is merely the first step in what can be a layered process. This document serves as a petition for review of an assessment by a local assessing official to the Property Tax Assessment Board of Appeals. However, to robustly support their case, taxpayers may find themselves needing additional forms and documents. The following list encompasses crucial materials that often accompany, supplement, or follow the initial petition to enhance an appeal's effectiveness:

Compiling a comprehensive packet with the State Of Indiana 130 Short Form and the relevant supporting documents serves two purposes. First, it strengthens the taxpayer's appeal by providing undeniable evidence of the property's value. Second, it streamlines the review process for the local assessing officials and the Property Tax Assessment Board of Appeals. Correctly utilized, these forms and documents collectively form a robust defense against unfair property tax assessments and lay the groundwork for a successful appeal.

The State of Indiana 130 Short Form is similar to other legal documents designed to initiate a review or appeal process concerning governmental decisions or assessments. This form, specific to property tax assessment appeals in Indiana, shares characteristics with several other documents across different jurisdictions and scopes. By understanding how this form compares to others, users can better navigate the legal processes involved in contesting or appealing various governmental assessments or decisions.

The Federal Tax Court Petition Form is one such document that bears similarity to the State of Indiana 130 Short Form. Both are formal appeals to a higher authority regarding tax assessments; however, the Federal Tax Court Petition is used for disputes with the IRS over federal tax assessments. Like the Indiana form, it requires detailed information about the taxpayer and the contested assessment, and it does not mandate the taxpayer to present an appraisal, although evidence supporting the taxpayer's claim is crucial. The structure of both forms is designed to guide individuals through the process of contesting assessments by providing step-by-step sections that require factual information about the dispute.

Local Property Assessment Appeal Forms, found in many counties and municipalities across the United States, also share similarities with the Indiana 130 Short Form. These local forms are used by property owners to challenge local property tax assessments they believe to be inaccurate or unfair. Similar to the Indiana form, local appeal forms typically require the property owner to provide specific details about the property and the reasons for believing the assessment is incorrect. Both sets of forms emphasize the importance of deadlines and procedural correctness to ensure the appeal is considered valid. Additionally, they facilitate a structured engagement between property owners and assessing bodies, aiming to resolve disagreements over value assessments without necessitating an appraisal.

The Zoning Appeal Form used in various jurisdictions to contest zoning decisions made by local planning or zoning boards, while not directly related to tax assessment, parallels the Indiana 130 Short Form in its function as a means to formally dispute a governmental decision. Both forms serve as the initiating paperwork that brings a dispute to the attention of a review board or authority. They require the filer to clearly state the grounds of their appeal and often include provisions for supporting documentation or evidence. This process underscores the role of structured legal forms in ensuring that individuals have a means to seek redress or challenge governmental actions that affect their property rights or financial obligations.

Filling out the State of Indiana Form 130, also known as the Petition for Review of Assessment by Local Assessing Official - Property Tax Assessment Board of Appeals, requires careful attention to detail and an understanding of the instructions provided. Below are nine essential dos and don'ts that will help ensure the process is completed correctly and efficiently.

Adhering to these guidelines will help streamline the process of filing a Form 130 in the State of Indiana, and ensure that your petition for review is duly considered by the assessing officials.

The State of Indiana 130 Short Form, officially known as the "Petition for Review of Assessment by Local Assessing Official - Property Tax Assessment Board of Appeals," is a crucial document for Indiana residents seeking to challenge their property tax assessments. Despite its significant role, there are several misconceptions surrounding this form and its process. Let's clarify some of these to ensure property owners are well-informed.

Misconception #1: Filing a State Form 130 guarantees a lower assessment. Filing this form initiates a review process; it does not ensure that the assessment will be reduced. The outcome can result in an increase, a decrease, or no change in property valuation.

Misconception #2: An appraisal is required to file Form 130. The process does not mandate a property appraisal for the review. Taxpayers can initiate and proceed with their review without this prerequisite, although additional documentation can support their case.

Misconception #3: Only the property owner can file Form 130. A representative, such as a tax representative or an attorney, can also file on behalf of the property owner, provided they have a notarized power of attorney or are an authorized corporate officer.

Misconception #4: There is only one deadline for all appeals. Depending on the circumstances, deadlines differ. For instance, appeals following a notice from a county or township official must be filed within 45 days of that notice. If no such notice was received, other deadlines apply.

Misconception #5: Filing is complex and aimed to deter appeals. While legal documents can be daunting, the State Form 130 is designed to be clear, simple, and understandable. Instructions are provided to assist in the completion and filing of this form.

Misconception #6: The decision of the Property Tax Assessment Board of Appeals is final. If unsatisfied with the decision, taxpayers have further recourse by filing a petition for review with the Indiana Board of Tax Review under specific guidelines.

Misconception #7: Filing an appeal is always beneficial. While it's every taxpayer's right to challenge their assessment, it's essential to consider the potential outcomes, including the possibility of an increased valuation. Professional advice can help weigh the merits of an appeal.

Understanding these misconceptions can help property owners navigate the process of appealing their tax assessments more effectively, ensuring they are prepared and informed every step of the way.

When filling out the State of Indiana Form 130 Short, a petition for the review of assessment by local assessing officials or the Property Tax Assessment Board of Appeals, taxpayers should keep several key points in mind:

Submitting the State of Indiana 130 Short form initiates a formal review process of a property assessment. The form provides the taxpayer and the assessing official a structured opportunity to present their views and evidence regarding the assessment. The outcome of this process can result in the increase, decrease, or maintenance of the original assessed value, directly impacting the property tax the owner is obligated to pay.

Cfa-1 - Advises on the inclusion of a list of banks or other depositories, emphasizing the importance of financial transparency in campaign activities.

State 54584 - Designed with your privacy in mind, this form requires detailed information to prevent unauthorized sharing.